{kind=link}

Cheques. Virtually every adult today would have come across this instrument while either paying for rent in advance or while finalizing a business deal or home loan. Those who are into a business most certainly have come across this important financial instrument in the business world.

It won’t be wrong to say that virtually everyone knows what a cheque is, except for millennials perhaps. It’s not their fault, though, as digital payments are the most popular method of payment in this age of technology due to which cheques are used quite less for a deposit or withdrawal of money.

What are Post-dated Cheques (PDC)

This article addresses the concept of cheques, Post-dated Cheques (PDC) and everything related to it. Let’s lay the foundation by understanding first what a simple bank cheque is.

Bank Cheques

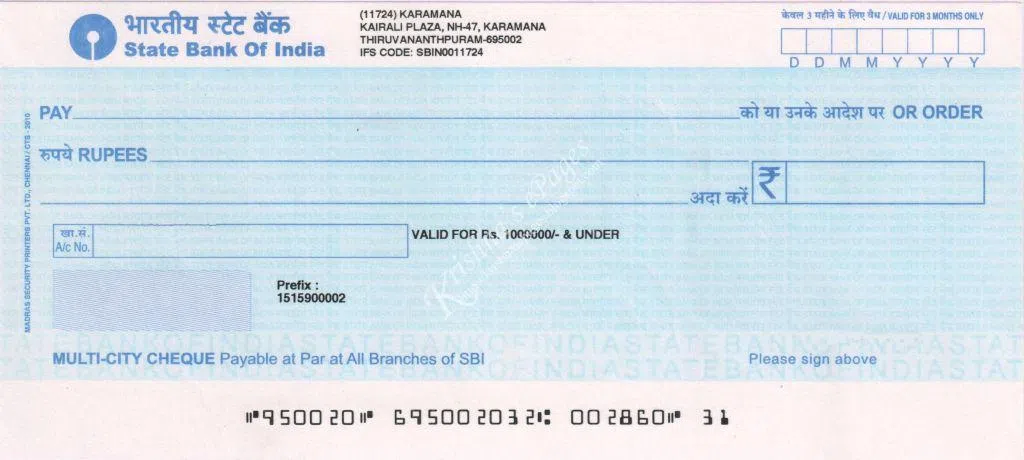

A cheque is defined as an instruction to the bank asking to pay a stated sum from the owner’s account to the cheque presenter or drawer. Cheques are written or printed in a specific format and in a form that is not easily replicable.

The respective banks print the cheques, and in some cases, customize them with the name or account number of the person holding an account with the bank. A sample cheque from the State Bank of India is shown below:

Components of a cheque

Before we dive into the details about Post-dated Cheques, let’s look at the components or parts of a cheque.

As you can see in the image of a sample cheque above, several blanks need to be filled in before you send the cheque to be honoured by the bank.

- The first one is the blank labelled Pay. This field will hold the name of the recipient or beneficiary of the cheque amount. This can be any name of an individual, business having an account or can be left blank. The name can also be the name of the owner of this account. In such cases, it becomes what is called a Self-Cheque. In the case of a self-cheque, the name needs to be specifically mentioned as Self.

- The second blank you see labelled Rupees needs to be filled in with the word form of the amount you wish to pay. For example, if the amount is Rs. 100, this field will contain the worded form of 100, which is “One Hundred”. This has to match with the numeral form in the box right after this blank.

- The bank usually prints out the box labelled account number before the cheque book is handed over to the customer.

- Finally, there is a place for a signature to the right bottom corner of the cheque. This has to be signed so that it should match your signature that is registered with the bank. If there is a difference between what you sign here and what is registered with the bank, the bank has the right to dishonour the cheque.

- The numbers at the bottom are printed in magnetic ink for clerical purposes when the cheques go through the bank for clearance. Those numbers are important for the bank to identify the bank code and bank account number.

- Lastly, you will have to fill in the date in the top right-hand corner. This is the date when the cheque will be honoured by the bank. This is an important aspect when it comes to PDC cheques.

Also Read: Learn All Necessary Information About Cross Cheques

What is a Post-dated cheque?

With the concept of cheques now behind us, it should be much easier to understand the concept of Post-dated Cheques.

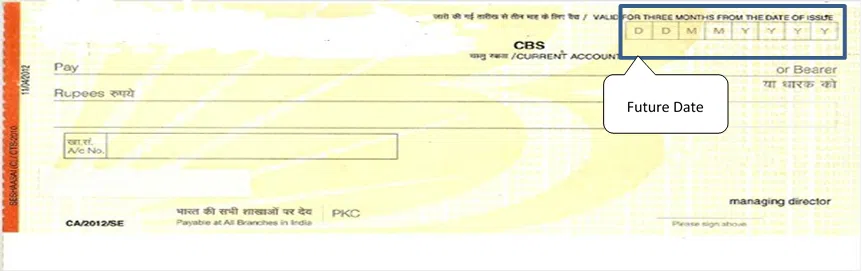

So, what is a PDC cheque? Post-dated cheques are normal cheques with a future date written on them. The cheques cannot be honoured by the banks before the date mentioned on the cheque.

- Strict guidelines have been framed around the issuance and honouring of post-dated cheques.

- Post-dated cheques are usually an instrument used to offset liability or to ensure payment of dues post-delivery of service. We shall get into the use cases of post-dated cheques in later sections.

Validity of a post-dated cheque

Post-dated cheques, like normal cheques, have a validity of 3 months from the date of issuance. The national bank of India, RBI (Reserve Bank of India), has reduced the validity period of all cheques from the previous 6 months to 3 months, effective April 1, 2012.

However, there is a small technicality. The 3 months are not counted in the number of days, but the date of issuance. For example, if the cheque was issued or is payable on 01 Jan 2023, the cheque will be valid till 31st of Mar 2023, irrespective of the number of days in between.

Use cases of Post-dated cheques

Post-dated cheques are usually issued in one of the below cases.

- If you do not have enough funds currently in your account, but you are sure that your bank account will have enough funds at a future date mentioned on the post dated cheque.

- If you would like to assure the service provider or supplier of goods that you will clear their dues after the service is rendered or goods are delivered. In such cases, the final payment may be negotiable depending on the quality of service or product.

- Financial institutions use Post dated cheques as a tool to ensure that borrowers do not default on repayment of loans.

Legal matters concerning Post-dated cheques

Section 138 of the Negotiable Instruments Act applies to cheques and post-dated cheques alike. Under Section 138, Post-dated cheques should have an amount written with a future date for withdrawl. There have been incidents where blank post dated cheques have been issued, and the courts have promptly rejected these as the cheques become a bill of exchange only if a certain amount is mentioned on the post-dated cheque.

It is important to note that a bounced or dishonoured cheque is considered a criminal offence, punishable by a jail term or fines under section 138 of the Negotiable Instruments Act.

Legal implications of dishonouring a post dated cheque

Under the provisions of the Negotiable Instruments Act, the legal penalty for the dishonour of a post dated cheque is:

- Jail term not more than 1yr.

- A fine equivalent to twice the amount specified on the post-dated cheque.

- Or both of the above.

As per the provisions of section 138 of the Negotiable Instruments Act, a legal notice should be issued within 30 days of the date the cheque bounced or was dishonoured.

In the absence of a valid response from the respondent, the concerned party must file a case within 45 days from the date of the legal notice.

Also Read: How to Cash a Cheque

Conclusion

Post dated cheques are a great way to enjoy products and services before you actually pay for such services and products. They can also be used as security for short term loans. It is also a quick way to continue business operations without having to stop for want of funds. It also ensures the quality of the product or service.