{kind=link}

If depreciation is credited to the depreciation allowance / accumulated depreciation account: This method does not credit the depreciation to the asset account but credits it to the accumulated depreciation account. The asset is recorded at cost minus the depreciation amount provided to date and credited to the depreciation allowance account on the balance sheet. Therefore, the sum of the asset’s original cost and the calculated depreciation can be obtained from the balance sheet. Alternatively, you can display the asset as a gross on the asset side and the depreciation allowance on the liability side.

Did you know?

Accumulated depreciation is a long-term contra asset account with a credit balance presented on the balance sheet under the heading Property, Plant, and Equipment. The amount of a long-term asset’s cost has been allocated since the asset was acquired.

What is Accumulated Depreciation?

The meaning of accumulated depreciation is the total depreciation expense allocated since the particular asset was first used. Accumulated depreciation is what type of account? This is a counter-investment account, sometimes referred to as a negative investment account, offsets the normally associated investment account.

Unlike traditional investment accounts, credits to counter-investment accounts increase their value, and debits decrease it. When a company reports depreciation, the same amount is credited to the accumulated depreciation account, allowing the company to view the asset’s cost and the total depreciation to date. The asset’s net book value is also included on the balance sheet. Depreciation allows companies to recover the cost of an asset when it is purchased.

Depreciable Assets

When an asset’s useful life expires or if an impairment charge is taken against the initial cost, it can attain full depreciation. However, this is less usual. When a corporation takes a full impairment charge against an asset, the asset is immediately depreciated to its salvage value (also known as terminal value or residual value). The depreciation method might be straight-line or accelerated (double-declining-balance or sum-of-year). The asset is fully depreciated on the company’s books when the accumulated depreciation equals the initial cost.

- A totally depreciated asset has reached the end of its useful life and has no worth other than its salvage value.

- After all, depreciation has been fully expensed, and the book value of an asset is known as salvage value.

- Unless it is disposed of, a completely depreciated asset on a company’s balance sheet will remain at its salvage value each year after its useful life.

Also Read: Straight Line Method of Depreciation – Straight Line Depreciation Formula

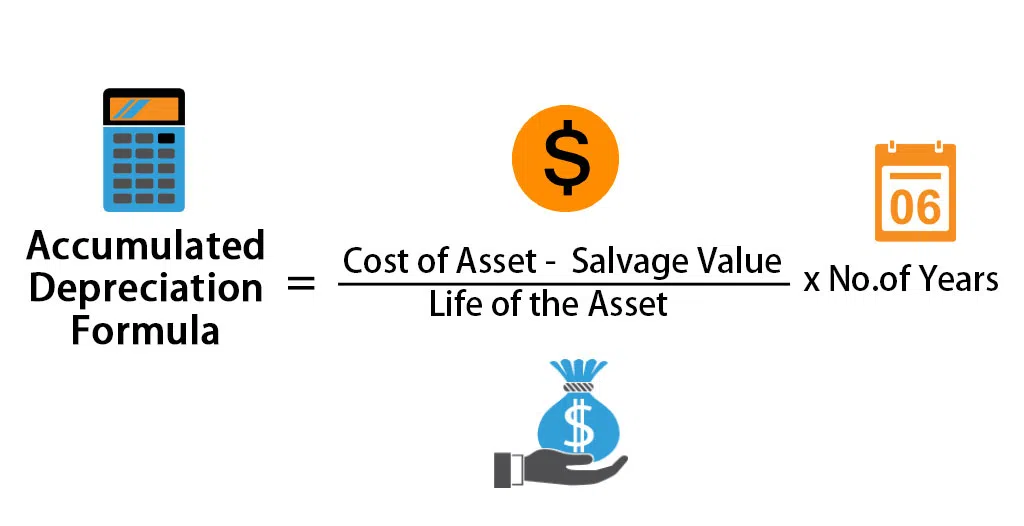

Formulas For Calculating Accumulated Depreciation

The Original Cost approach and the Written Down Value method are the two main methods for calculating an asset’s Accumulated Depreciation or two major types of Charging depreciation.

-

Original Cost approach

The primary approach for computing accumulated Depreciation is the Original Cost method.

This method’s formula is as follows:

(Asset cost – Expected salvage value) / Years of Expected Use.

The asset’s cost represents the asset’s original value when you originally acquired it, but the expected salvage value shows its total expected value once it’s no longer usable. The number of years you expect the asset to last is represented by the estimated years of use.

-

Written Down Value Method

The Written Down Value Method is critical for capturing most of an asset’s Depreciation early in its useful life. This means that a corporation charges most of an asset’s depreciation expenses in the early years of its use, beginning when the asset is acquired. The corporation estimates a reduction in Depreciation of the asset’s value as it loses usability and value over time.

To compute accumulated Depreciation for years, use the following essential Written Down Value Formula:

Depreciation factor x (1 / Asset Lifespan) x Remaining Value = Total yearly depreciation

Divide the result by 12 to get this number monthly. Multiply by 1.5 or 2 if you want to assume a higher Depreciation rate.

What Is Depreciable Property and How Does It Work?

Assets that are subject to depreciation registration for tax and accounting purposes in accordance with the IRS standard are called depreciable assets. Vehicles, real estate (excluding land), computers and office equipment, machinery and heavy equipment are examples of depreciable assets. Long-term assets are depreciable assets.

Some Important Terms

Depreciation:- Measures asset wear and tear due to uses of time or obsolescence due to technological and market changes. It is written off as an expense over the asset’s expected useful life. All tangible long term assets with a predetermined useful life are subject to Depreciation. For example, a machine’s usable life is estimated, and the machine’s cost is written down over that anticipated useful life. The productive life of the land, on the other hand, is frequently infinite. This does not reduce the value.

Amortization: is a systematic and gradual depreciation over the expected useful life of an intangible asset. Intangible assets such as patents and copyrights acquire goodwill and amortize it over their useful life.

Depletion: Depletion charges are a metric used to measure the depletion of wasted assets such as quests, material extraction from mines, etc. Extraction reduces the amount of material available. For example, mining coal from a mine is a diminishing supply of coal.

Causes of Accumulated Depreciation

Use of Physical Assets: Use of physical assets leads to wear and thus loss of value.

The Outflow of Time: Some assets, like leases, have a finite lifespan. After the end of its useful life, the asset expires. Other assets, such as plants and machinery, may not have a finite lifespan. In their case, lifespan is estimated.

Obsolescence: Older machines may need to be deprecated when newer, cheaper machines become available, even if they are still operational. This shortens the useful life of the asset.

Accident: Accidental damage can be permanent but not continuous and gradual.

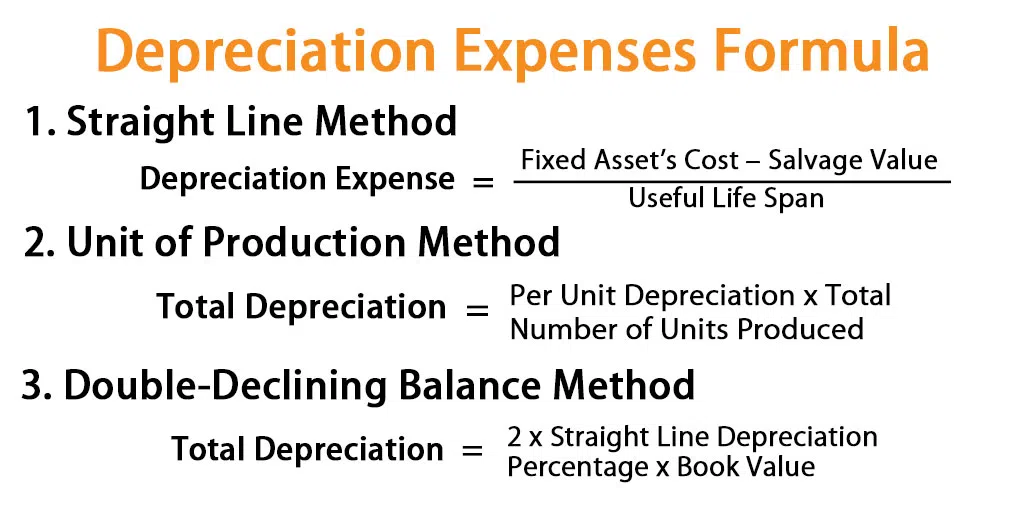

Methods of Accumulated Depreciation

Following are the three important methods of accumulated depreciation:

-

Straight-Line Method

(Asset cost – Expected salvage value) / Expected years of use

-

Declining Balance Method

Total yearly depreciation = Depreciation factor x (1 / Lifespan of asset) x Remaining value

-

Double-Declining Balance Depreciation Method

Total yearly depreciation = 2 x Depreciation factor x (1 / Lifespan of asset) x Remaining value

Also Read: Trial Balance: Rules Explained With Examples

The Objective Of Providing Depreciation Or Accumulated Depreciation

Depreciation is provided with the following objectives:-

- To Determine Correct Profit or Loss:- Depreciation is an operating expense and is therefore recorded in revenue. The income statement for an accounting period does not constitute an accurate and impartial assessment of its profitability (i.e. net income/loss) unless it is recorded as an expense.

- To show a True and Fair View of the Financial Position:- If depreciation is not taken into account, the asset will be valued higher. As a result, the position statement (balance sheet) does not reflect the financial situation accurately.

- To determine the Cost of Production:- When estimating the cost of manufacturing, Depreciation is taken into account. If Depreciation is not taken into account, the production cost will be reduced by the amount of Depreciation.

- To provide funds for replacement: Depreciation is deductible. Once the depreciation expense is calculated, the amount remains in the company and can be used to replace property, plant and equipment after the expected useful life.

- To comply with legal provisions:

Depreciation must comply with the Companies Act and Income Tax Act.

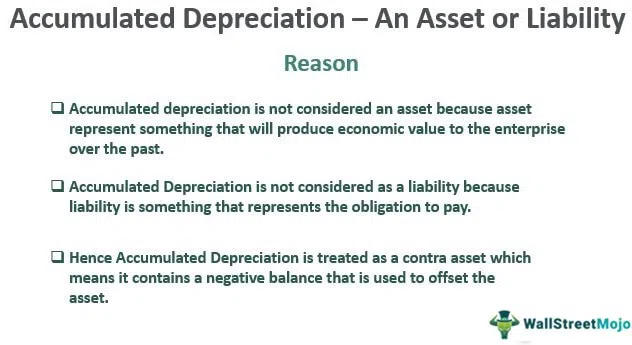

Is Accumulated Depreciation a Liability or an Asset?

Accumulated depreciation is credited and recorded in the asset-to-asset account, which reduces the total value of fixed assets. Therefore, there is no distinction between assets and liabilities.

Conclusion

Depreciation costs are non-cash costs. Accumulated depreciation or provision for depreciation indicates the total depreciation provided to the asset so far. On the balance sheet, the asset is recorded at cost minus the depreciation expense provided to date and credited to the depreciation allowance account. Offset asset accounts, or negative asset accounts, usually balance the paired asset accounts. The total depreciation expense resulting from individual assets since the start of operation is called the accumulated depreciation amount. Some assets, like leases, have a finite lifespan, and when they expire, the assets no longer exist.

Now keep track of your cash flow and manage your incomes and expenses with ease by using the Cashbook app by Legaltree.