{kind=link}

What is a trial balance? The trial balance is a summation of or list of credit and debit balances drawn from the many ledger accounts like the bank balance, cash book etc. The cardinal rule of the trial balance is that the total of the trial balance debit and credit accounts and ba lances taken from the ledgers should be the same or tallied. This is because every transaction has a credit and debit entry or an effect with dual consequences. When an accounting period ends or at the end of each month when the ledgers are tallied and duly extracted, it is the trial balance that tests whether the total credits and total debits are in a systematic pattern or not. If not, there is an error or inaccuracy in the ledger entries. It is the primary account statement from which several financial statements like the Balance sheet or P&L or Trading and Profit & Loss account and more are prepared.

The Objectives of a Trial Balance:

The trial balance is used to prepare financial statements from the ledger and journal entries. It is the basis for preparing the financial statements like balance sheet etc., and the final P&L accounts. The trial balance format and its objectives include:

- Assessing the ledger accounts’ arithmetical accuracy when the total credit is equal to the total debt.

- Locating ledger and journal errors or inefficiencies in the many stages of the accounting system. Such errors may arise when posting the ledger or journal accounts with the many entries, calculation or manual errors in entering values, totalling the subsidiary ledgers/ journals, trial balance posting errors, etc.

- Preparing the various financial statements like the P&L account, balance sheet, other financial statements, accounting records, etc.

- Expenses and income entries are taken from ledger accounts for the P&L account,

- Journal entries are required for the balance sheet.

Thus, the trial balance is the foundational bridge between the financial statements and the various accounting records.

Trial Balance Features:

- The trial balance is a statement of accounts and not an account by itself. It is also never a part of the final financial statements.

- It contains the summation of credit and debit balances drawn from the many ledger accounts in a trial balance format.

- Its objective is to prove the arithmetic accuracy of its entries since, in a Trial balance, the credit and debit balances are equal. It does not verify the inaccuracies, however, which requires an audit to prove inaccuracies in the credit/debit balances.

- Every accounting year has a Trial balance drawn at its end. If needed, such trial balance sheets can also be drawn monthly, half-yearly, quarterly, or even weekly.

- It is the foundation stone of all account statements and the connecting bridge between the Profit and Loss Account, Books of accounts, and the Balance sheet.

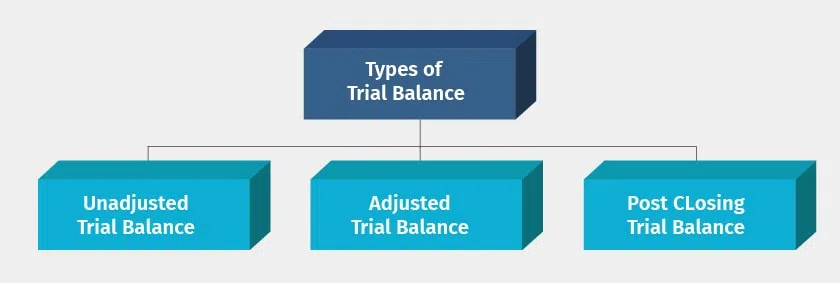

Trial balance types:

There are three different types of trial balances drawn at various accounting cycle stages.

The 3 trial balances are-

- Adjusted Trial Balance.

- Unadjusted Trial Balance.

- Post closure Trial Balance.

Rules in drawing the Trial Balance:

Here are the rules of a trial balance.

- All liabilities must be reflected on the credit side and assets reflected on the debit side.

- Gains and income must be reflected on the credit side of a trial balance.

- Expenses must be reflected on the debit side of the trial balance.

Also Read: Profit and Loss, Account and Statement

Errors in a Trial Balance:

The Trial Balance ensures the debit and credit entries match with arithmetical accuracy but they do not portray the accuracy of the ledger account. Let’s explore some of the errors that can occur in a trial balance.

- Errors of Commission: These errors occur when the correct amount is in the right class of accounts but the wrong account. For example, Mr C sold goods worth Rs 1000/- to Mr X and entered them as Goods Sold in the account of Mr Y.

- Errors of Omission: These errors are errors where a transaction is not reflected or completely omitted. For example, if goods worth Rs 1000/- were sold to Mr B and completely omitted from the books of accounts, the trial balance will still show the debits and credits as matched since both the debit and credit for Rs 1000/- are understated in the Trial Balance.

- Errors of Principle: These transactions reflect the correct amount but on the wrong side and class of accounts. For example, the purchase of a fixed asset car is wrongly reflected in the Expenses Account for motor vehicles, a revenue expense account.

- Compensating Errors: These errors occur when two or more same value accounts occur on both the credit and debit sides. For example, instead of debiting the Fixed Asset account by Rs 50,000/-, the Sales (credit account) is provided Rs 50,000/-.

- Reversal of entries: The errors occur due to the correct accounts being recorded but on the wrong side. The trial balance will still balance in this case. For example, Rs 20,000/- in cash from Mr A was wrongly debited to their account, and a credit entry passed for Cash Book.

- Errors of transposition: These entries occur when the numerical values of the right entry are wrongly written with transposed values. For example, Rs 4235/- was wrongly written instead of 4,523/-.

Steps to prepare the trial balance sheet:

The trial balance is the first step of preparing the final financial accounts, where the statements of the closing balance from general ledgers accounts are considered. The steps to prepare the trial balance are:

- Firstly prepare the ledger accounts and the closing balances of every account in it. For example, the bank overdraft in trial balance, the commission received in trial balance and general expenses in final accounts, among the others.

- Now post these balances into the trial balance’s credit and debit columns.

- Expenses and assets are accounted for as debit balances, while income and liabilities are considered credit balances.

- Next, calculate the total debit and credit balances.

- If the trial balance is accurate, the sum of credit and debit balances should be equal.

- In case of any differences in the balances, you must undertake trial balance error rectification through an audit of the accounts.

Trial balance format and example:

Take a look at the below format of a trial balance of a firm.

As shown above, the ledger accounts are mentioned in the first column, and their various entries are shown as credit or debit entries in the respective columns.

Format of trial balance:

Trial Balance of ABC Ltd as on dd/mm//yy.

|

SI No |

Particulars |

L.F |

Amount (Rs)Dr |

Amount (Rs)Cr |

Trial Balance Example:

ABC Ltd Trial Balance on 31- March 2020 (in Dollars)

|

Accounts |

Debit (Dr) |

Credit (Cr) |

|

Cash |

1,20,280 |

– |

|

Accounts Receivable |

9,500 |

– |

|

Office Expenses |

2,500 |

– |

|

Prepaid Rent |

800 |

– |

|

Prepaid Insurance |

220 |

– |

|

Office furniture and equipment |

15,000 |

– |

|

Bank loan |

– |

15,000 |

|

Accounts Payable |

– |

5,000 |

|

Unearned Revenues |

– |

9,500 |

|

Capital |

– |

1,21,200 |

|

Drawings |

5,000 |

– |

|

Commission Revenue |

– |

12,500 |

|

Salary Expenses |

9,900 |

– |

|

Total |

163,200 |

163,200 |

Trial Balance Forms:

The trial balance can be drawn in the below two forms. Namely,

- Ledger Form where the trial balance is cast in the form of an account with credit and debit sides. Both sides have the first column having the account name, amount column, folio column, etc.

- Journal Form where the trial balance takes the journal form with a column for serial numbering, account name, debit/credit amounts, ledger folio details, etc., including the page number on which the account is entered in the ledgers.

However, due to the dual nature of entries with each of the debtors in trial balance having a corresponding credit entry and vice versa, the trial balance, when right, must always tally.

Trial balance items list:

As seen in the format of the Trial Balance, there are several credit and debit accounts accounted for therein. Here is a quick table to help classify them.

|

Debit Side |

Credit Side |

|

Total Assets (Cash in bank/ hand, Buildings and Land, Inventory, Plant and Machinery, and more.) Expenses (Freight, inward carriage expenses, rents, salary, rebates, Commission, etc.) Sundry debtors in the trial balance Losses (Inward returns, bad debts, depreciation, debits to P&L A/c, etc.) Purchases |

Total liabilities (Unsecured/ Secured loans, Bank overdrafts, mortgage loans, outstanding bills and expenses payable, and more.) Reserves in funds, depreciation provisions, general reserves, accumulated depreciation on plant and machinery, etc. Gains (Outward returns, recovered bad debts, discount received, credits to P&L, etc.) Sales |

Modern-day advances in accounting and Trial Balances:

The trial balance helps detect any errors accurately. But, with business needs becoming more diverse, financial statements are needed to be in alignment with business health and funding so that effective decisions can be made. Most businesses use advanced accounting software like Tally Prime, Tally ERP 9, etc., to maintain their books, draw financial reports and statements, and use financial data for analytical reports. Hence, you need not ever have to balance credits and debits anymore to draw Trial balance sheets, as TallyPrime, an accounting software, ensures the matching of credits and debits when recording transactions automatically. This is also a more efficient, reliable, accurate way of recording transactions digitally while saving effort, time, resources, and more.

Also Read: Double Entry System of Accounting

Conclusion:

In this article, we have seen how the trial balance is prepared, what is trial balance in Tally with trial balance examples.