{kind=link}

Share capital refers to the money invested in the company by its founders or owners in a multi-owner structure. It represents the percentage of the total amount of money invested in the company.

Shareholders are also known as company members. They own shares of the company and have the right to participate in management decisions.

The shareholders of a company have the right to receive dividends and profits. Authorised capital refers to the amount that a company is allowed to issue. The number of shares a company can issue is regulated in the Memorandum of Association. It can also be called “normal capital”.

Now, let’s read the article to understand the intricacies.

Did You Know?

The proceeds from stock sales are listed at the nominal par value, while the “additional pay-in capital” line represents the actual price paid for the shares on a balance sheet.

What is Share Capital?

What is Share Capital?

Share capital is a company’s amount of money legally raised through the sale of shares, and it includes both common and preferred stocks. In most cases, the share capital is increased through additional public offerings.

A company can raise more money by making more stock available, but its authorised share capital is the maximum amount it can raise in a public offering. The proceeds from these sales are listed as “additional paid-in capital.” This amount indicates the real price paid for the stock.

There are many different types of share capital, but the two most common types are registered and authorised.

Also Read: Know How To Calculate Cost of Capital With Examples

What are the Types of Share Capital?

There are several different types of share capital, including subscribed capital and Unissued Share Capital. Understanding the difference between each will help you decide if your business needs it. Check the 8 types mentioned below:

Authorised Share Capital

A company’s authorised share capital is the number of shares it is permitted to issue. It is limited to a certain amount and can only be increased with shareholder approval.

Its authorised share capital is usually higher than the total number of shares. Increasing the authorised capital will allow a company to issue more shares and may even change the balance of power between its shareholders and its creditors.

A company can issue new shares for several different reasons, including raising capital or acquiring another company. Some companies may issue stock incentives for their employees.

Unissued Share Capital

Unissued shares are stock that a company has not yet issued to the general public or employees. Also, the unissued stock is normally held in a company’s treasury and has no bearing on the firm’s shareholders.

A firm can raise unissued share capital through early-stage investors, reinvesting profits, or borrowing from banks. The stock can be sold in the future to pay off debt or to raise money for new investments.

Unissued shares have a low value and are controlled by the company’s Board of Directors. Unissued shares might be sold at a bargain or allocated to other shareholders for consideration. A majority of a company’s shareholders can receive unissued stock.

Directors may distribute unissued shares to a minority of present shareholders despite being under the control of the company’s shareholders. This technique, however, should not depreciate the value of current shareholders’ shares.

In other words, if a firm has more shares than a particular number of authorised shares, the float will likely be higher than the total number of unissued shares.

It is not uncommon for a company to hold a large percentage of its unissued shares in treasury. These shares are not available for trading on the open market, but they are retained in the company to make sure it is ready to be sold.

Issued Share Capital

Issued share capital is the amount of stock a company issues to its shareholders. This capital may include a mix of shares: common equity and preferred. Issued share capital is an important component of a company’s balance sheet.

It’s used to figure out how much the company’s stock is worth. A corporation may, for example, issue one hundred shares of ₹10. One hundred shares would cost ₹1,500 if all of the company’s stockholders bought one. The corporation would have raised ₹1,000 from the initial stock sale, with the remainder being surplus.

Subscribed Capital

A company’s Issued share capital must be equal to its registered capital, and a portion of this is called subscribed capital. Shareholders subscribe to a company’s shares and pay for them in instalments.

They never pay the full face value of their shares at one time, but only part of it. This is known as the capital. A company may issue a portion of its subscribed capital and call the remaining portion uncalled.

A company’s subscribed capital is the part of its issued capital accepted by the public. It’s a way for the public to show their interest in a company. This capital is not issued to the public in one go, and the company may choose to issue additional shares from time to time.

Paid-Up Capital

Paid-Up Capital is the amount of money received by a company from the issue of shares. Normally, a company will raise funds by issuing fresh share capital. This fresh share capital becomes a part of the company’s paid-up capital.

Under the Companies Act, 2013, companies’ minimum paid-up capital requirement is ₹1 lakh. However, if the company does not require a minimum paid-up capital, its shares can be very low.

Paid-Up Capital is a crucial metric for investors when performing fundamental analysis. A company with a high paid-up capital may have lower debt than its peers.

Called-Up Capital

Called-Up Capital is the cash an organisation pays to its investors, including partial payments. It is listed under the shareholders’ equity portion of the balance sheet. Fully paid-up organisations do not need borrowed money.

Instead, they can sell additional shares of stock to attract new investors. While called-up capital does not guarantee the return of investments, it can be a useful tool for companies that need ad-hoc funding.

When a firm issues shares, the shareholders are ‘called up’ to pay the remaining balance. A call-up is something like this. The shareholders are still entitled to the full amount if the firm issuing the shares does not expect to receive it all at once.

However, a called-up capital provides for more flexibility in the investment term and the payment terms. It also allows investors to pay less for their shares.

Reserve Share Capital

Reserve share capital refers to the number of shares a company cannot call upon in case of liquidation. It is part of the issuer’s subscribed capital and comes in two forms: fully paid up shares and partially paid shares.

The latter are generally held in reserve pending liquidation. In some cases, a company may use its reserve share capital to repay shareholders in case of insolvency and is considered the “initial paid-up capital” for a company.

Another term for Reserve share capital is Capital Reserve. This refers to the part of a company’s reserves that cannot be distributed as dividends. A company may have an excess of capital reserves.

A company may use the surplus to pay dividends or purchase new stock, but this should not be the only source of capital for a new venture. Equity funds can be acquired from third-party investors, friends, or family members in these cases. The company may use personal resources to provide equity funds in some cases.

Uncalled Share Capital

Uncalled share capital is a portion of a company’s subscribed capital that has not been paid for. This capital is not recorded in the company’s books as a debt. The company may reduce this capital to zero by paying back some of the shares.

This action releases the shareholder from any liability on the unpaid capital. The company may also return part of the unpaid share capital to the shareholders. In some cases, the company may pay off some of this unpaid capital because it may be called up again at a later date.

The uncalled share capital represents the amount of subscribed share capital not called up for payment. In most cases, companies call up a portion of their share capital at the allotment, leaving the remainder of the share price unpaid.

The company must make the remaining portion of the unpaid share capital available to raise further finance. Therefore, it is important to understand the difference between called-up and uncalled share capital.

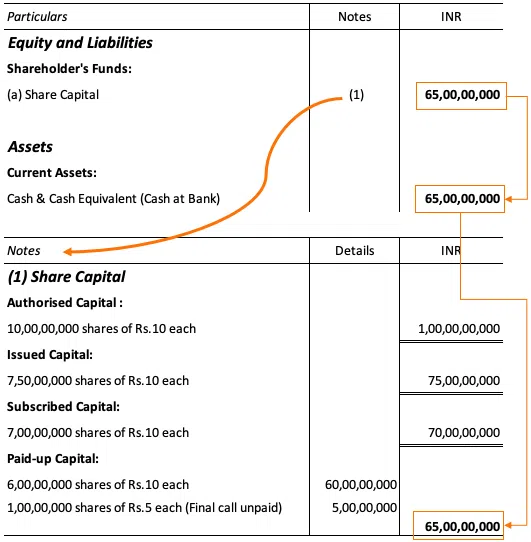

The Balance Sheet’s Representation of Share Capital

A company’s capital is shown on the Liabilities side of its Balance Sheet. This is because a corporation is a legal entity that owes its capital to its owners and investors. Under the heading Shareholders Fund, you’ll find share capital.

With the help of an example, we’ll show you how to display share capital in the Balance Sheet:

Also Read: How to Register a Private Limited Company Online?

Share Capital BreakDown

The money raised by selling common or preferred shares is referred to as a company’s share capital. The maximum amount a firm can raise in a public offering is known as authorised share capital. In order to expand the share capital on its balance sheet, a corporation may choose to make a new stock offer.

On a balance sheet, the stock sales profits are recorded at their nominal par value, but the “extra paid-in capital” line reflects the real price paid for the shares over par.

Only payments made directly from the corporation for acquisitions are included in the amount of share capital published by a company. The company’s share capital is unaffected by later sales and acquisitions of such instruments, as well as rising or declining open market rates.

After its Initial Public Offering, a firm may choose to have multiple public offerings (IPO). The revenues from those later transactions would be used to boost the company’s share capital.

Other types of equity accounts are distinct from share capital. This equity account relates only to the amount “paid in” by investors and shareholders. It is the difference between the par value of a stock and the price that investors actually paid for it, as the name “extra paid-in capital” implies.

Conclusion

Share capital refers to money generated by the sale of shares for the general public, referred to as “shareholders” of the business. It is among the main sources of capital finance for those Joint Stock companies. Capital raising via the issue of shares comes with advantages and disadvantages, which companies must weigh before making financing decisions.

Follow Legal Tree for the latest updates, news blogs, and articles related to micro, small and medium businesses (MSMEs), business tips, income tax, GST, salary, and accounting.