{kind=link}

We often come across the term budget, and you may have heard it from your parents or friends. What is a budget? A budget is an estimate of income and expenditures for a given period and is often created and updated regularly. An individual, a group of people, a company, a government, or any entity that manages the money supply can have budgets.

Capital budgeting is essential if you want to control your spending each month, stay ready for life’s unforeseen events, and also be able to buy expensive products without falling into debt. It doesn’t have to be tedious, and you don’t have to be brilliant at mathematics. Moreover, keeping track of your income and expenses doesn’t imply you can’t buy the items you want.

Simply put, it means you’ll be more in charge of your finances and in a position to understand and evaluate where your money is going. A production budget is not a place where you can lock yourself away from your cash. Instead, it’s a technique you employ to ensure your future life is superior to your present, at least monetarily.

Did you know? RK Shanmukham Chetty, the finance minister at the time of India’s independence, delivered Independent India’s first budget on November 26, 1947.

What Comprises a Budget?

A budget comprises a spending plan based on income and expenses. In other words, it’s a projection of your income and expenses for a specific time frame, like a month or a year. A surplus business budget indicates profits are predicted, and a balanced budget indicates revenues are projected to equal expenditures. A deficit budget indicates expenses will grow more than revenues.

The term “budget” comes from the English word “bowgette,” which in turn is derived from the French word “bougette,” implying a leather sack. The Union Budget is a declaration of the estimated receipts and expenditures of the government for a specific year, as per Article 112 of the Indian Constitution.

Also Read: Costing: Definition, Objectives, and Advantages

What is the Production Budget?

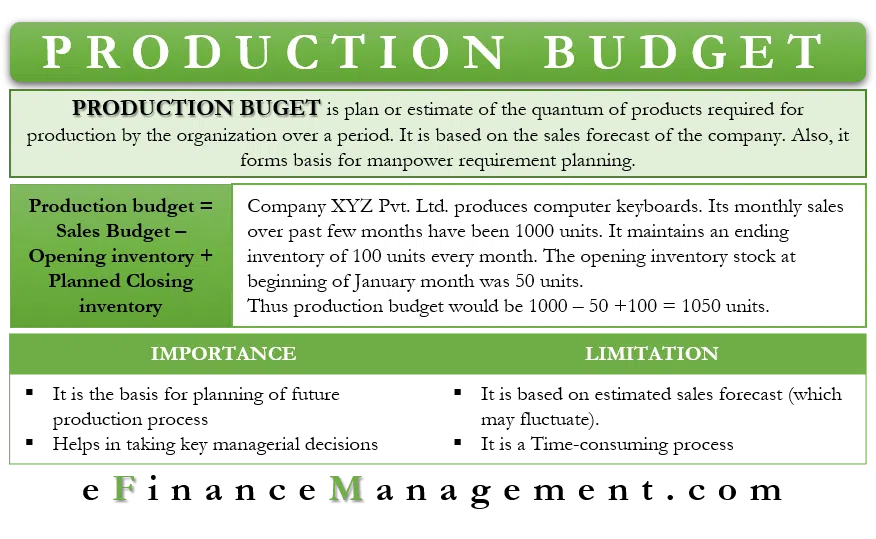

The sales forecast and the anticipated amount of units of the commodity to be manufactured and its inventory to be on hand are combined to create the production budget. It determines the number of products that must be made (usually as emergency stock to cover for unanticipated increases in demand).

The production budget is often created in a material requirement analysis environment, which uses a “push” manufacturing approach. A budget is a financial plan for a predetermined time frame, such as a month, quarter, or year. Its creation and maintenance is a crucial task for every business and estimates various metrics, including sales, income, expenditure, etc. An estimate or plan of how many products the organisation will need to produce over a certain period is the production budget meaning. It is a projection of what the business will sell in the upcoming time frame, depending on the sales forecast.

The production budget also considers the target inventory level a business wishes to have to cover emergencies and prevent product shortages. It serves as the foundation for creating cost budgets for acquiring raw materials and other consumables. This sort of budget is for business operations. It serves as the foundation for determining how many people should be hired.

Also Read: Meaning of Accountancy and How it Differs From Accounting

Example of a Production Budget

Based on anticipated future sales figures, managers utilise the production budget to determine how many items they will need to manufacture throughout subsequent periods. In addition, they use this data as a planning tool for upcoming scheduling, machine times, and production methods.

Production managers must project future demands and organise the workflow to ensure everything is produced on time and there aren’t any long wait times or downtimes. Let us look at a production budget example.

Three different activity periods are compared in a typical production budget. Depending on how long the management needs to estimate their plans, these time frames could be weeks, months, or even years. A straightforward equation determines the units manufactured during the period in the report. It starts by multiplying the planned sales units for the following period by the proportion of projected sales to inventories.

We now have the budgeted ending inventory expressed in units. The number of units must be produced based on the anticipated sales figures, and the intended closing stock balance can then be determined by adding the budgeted sales items for the relevant decade and deducting the opening inventory.

Also Read: Understanding the Limitations of Accounting in Detail | Legaltree

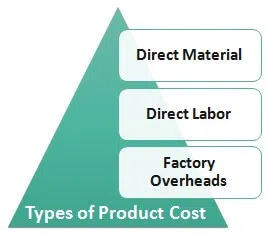

Types of a Production Cost Budget

The production cost budget can be of three types. These are laid down below:

-

Direct Materials Budget

The number of direct materials needed to meet production demands is estimated by the budget for direct materials, and it is included in the organisation’s material requirement planning (MRP). The quantities of raw materials are calculated for the Direct Materials Budget based on the year’s production goals and closing inventory.

-

Direct Labour Budget

The Direct Labor Budget, as its name implies, deals with the expense of direct labour used in manufacturing, assembly, or service. This budget details how much direct labour will cost and how many hours it will take to produce or provide service. We might say a budget like this enables a business to control the workforce it requires. Employees that perform factory floor work to create a product are referred to as direct workers.

-

Production(Factory) Overhead Budget

All manufacturing expenses, except direct labour and material costs, are included in the production or manufacturing overhead budget. The data from this budget is added to the master budget’s cost of goods sold item. The sum of all expenditures in this budget is translated into an overhead budget for each unit. The cost of the final finished goods inventory is calculated from the overhead budget per unit and then shown on the projected balance sheet. Given it may include a significant portion of a company’s total spending, this budget’s information is among the most crucial of the different departmental budget models.

Compared to a firm that has been around for a while and has access to historical data and expertise, it is far more difficult for a company that just got started to predict the numbers for the production budget.

Also Read: What Are Different Types of Accounting Explained With Examples & Importance

How is the Production Budget Estimated and Calculated?

The production budget is disclosed either quarterly or per month basis. The production budget’s fundamental calculation is as follows:

Forecasted unit sales plus planned finished goods closing stock balance equals the total production required, and less opening-closing inventory balance gives the products to be manufactured.

Production budget = Budgeted sales units – Opening stock of finished goods + Closing stock of finished goods.

The forecast data is grouped into broad categories of items with common characteristics since it can be challenging to generate a thorough production budget that includes a prediction for every variation of a commodity a company sells.

The intended level of ending finished products inventory is debatable since either too much or too little might result in obsolete stock that must be discarded at a loss or lost sales when consumers desire immediate delivery.

Also Read: What is the Difference Between Auditing and Accounting? – Learn Auditing and Accounting

Conclusion:

A production budget forms the basis of planning the production process in the future. Planning begins with a well-designed production budget in any firm. It disregards production costs. As a result, it makes possible the use of machines and efficient manufacturing process scheduling. For the management, the production budget is the key to the procurement budget, which allows managers to calculate how much they can spend to obtain the goods or services needed. The manufacturing budget is the only factor that determines what supplies and consumables can be purchased. Important aspects like hiring new employees are also influenced by how much manufacturing is possible for the business.

However, the production cost budget is solely based on projected sales estimates. Additionally, keeping an inventory is an individual choice and open to major changes, and these numbers merely reflect the management’s assessment. Unexpected changes in the supply or demand for the product, shifts in the state of the economy, a recession, or even competition might cause disruptions.

The production budget projects the company’s output and sets goals for employees to meet to produce the desired output while incurring the fewest costs efficiently. Despite the restrictions, budgets continue to serve as the blueprint for future action. In addition to that, all budgets are predicated on a set of assumptions and reflect a plan or estimation for the future.

Follow Legal Tree for the latest updates, news blogs, and articles related to micro, small and medium businesses (MSMEs), business tips, income tax, GST, salary, and accounting.