{kind=link}

The Pradhan Mantri Mudra Yojana provides MUDRA Loans. Micro-Units Developmental and Refinance Agency is known by the initials MUDRA. As per the Shishu, Kishor, and Tarun categories of the mudra loan, borrowers can obtain business loans via this programme in the range of ₹50,000 to upto ₹10 lakhs.

Did you know?

The mudra scheme’s target was ₹3 lakh crores for the financial year 2022.

What is the Pradhan Mantri Mudra Yojana Scheme?

On April 8, 2015, Prime Minister Narendra Modi introduced the Pradhan Mantri Mudra Yojana, which aims to give non-corporate organizations loans up to ₹10 lakhs. Under Pradhan Mantri Mudra Yojna, MUDRA Loan makes financing the credit needs of all non-farm income-generating enterprises easier. This program’s primary goal is to lend money to small and medium-sized businesses that aren’t corporations or agricultural.

Following agriculture, non-corporate micro-enterprises account for the majority of the job possibilities in the nation, which are thought to number in the range of 10 crores and impact the lives of 50 crore Indians. Popularly referred to as Proprietary or Own Account Enterprises (OAE) enterprises, they primarily engage in manufacturing, trade, logistics, and distribution. Despite being the biggest unorganised company ecosystem in the world, this industry is correctly referred to be the nation’s economic bastion. Under the sponsorship of PMMY, the MUDRA programme seeks to convert this sizable industry into an institutional credit hub, making it a potent driver of GDP development and job creation.

Also Read: Learn about Short Term Loans – Short Term Loan Period, Advances & Types

Pradhan Mantri Mudra Loan Eligibility – Check here:

Types of Companies

- Boards for Railroad Recruitment

- Micro Finance Companies

- Business banks

- Financial institutions that are not banks

- Banks with Small Finances

Types of Industries:

- Commercial vendors

- Shopkeepers

- Agriculture industry

- Small-scale producers

- Self-employed businesspeople

- Repair and restoration businesses

- Service-based businesses

- Food production industry

- Handicraftsmen

Types of Loans Under the MUDRA Scheme

Mudra loans are designed for small business entities. A mudra loan can be applied for by anybody who owns a small business. The MUDRA Loan primarily offers two forms of financing:

1. A Microcredit Programme.

It is primarily offered to various microenterprises and small companies by microfinance organisations, which offer loans up to ₹1 lakh in total.

2. Refinance Initiative for Banks.

For MUDRA refinancing assistance, various banks, including Commercial Banks, Municipal Rural Banks, Small Financial institutions, and NBFCs, are permitted. This refinancing is accessible up to a maximum of ₹10 lakhs per business and mainly applies to term loans and working capital loans. The plan is divided into 3 categories to make it simpler:

Shishu:

Start-up businesses can apply for a mortgage under this category for up to ₹50,000. The interest rate would be between 10% and 12%

Kishor:

Unestablished enterprises can apply for a loan under this category and pay a rate of interest of 14% – 17% for loan amounts ranging from ₹50,000 to ₹5 lakhs.

Tarun:

Applying for a loan under this class with the financing of up to ₹10 lakhs is an option for established firms that want to expand their current unit. The interest rate range is over 16%.

|

Category |

Loan Amount |

Rate of Interest |

|

Shishu |

₹50,000 |

10-12% |

|

Kishor |

₹50,000 to ₹5 lakhs |

14% – 17% |

|

Tarun |

up to ₹10 lakhs |

16% |

Purpose of Pradhan Mantri Mudra Loan Yojana

MUDRA loans can be obtained for several purposes that generate revenue and new jobs. The following are the primary uses of Mudra loans:

- Business loans for retailers, wholesalers, distributors, and other service-related businesses.

- Financing for small business units’ machinery

- Using MUDRA cards, obtain working capital.

- Loans for transport vehicles.

- One can apply for a Mudra Loan if they are engaged in agri-allied non-farm income-generating businesses like poultry farming, beekeeping, fish farming, etc.

- A Mudra Loan is available to those who utilise tractors, tillers, and two-wheelers for business purposes.

Also Read: Cash Credit Loan – Eligibility, Interest Rate, Features & Benefits

How to Apply for a Mudra loan?

Offline

- Visit a bank or NBFC that has PMMY authorization.

- Make sure you have a unique business strategy.

- Request the Mudra loan registration form, then complete it with the necessary information.

- Send the application form, two passport-size photos, and other paperwork.

Online

Anyone interested in applying for a Mudra Loan can do so by going to the authorised banks’ official websites. Depending on your demands and the size of your operations, you must fill out the online application for the Shishu, Kishore, or Tarun loan programme. The straightforward methods to apply for a Mudra loan online are listed below:

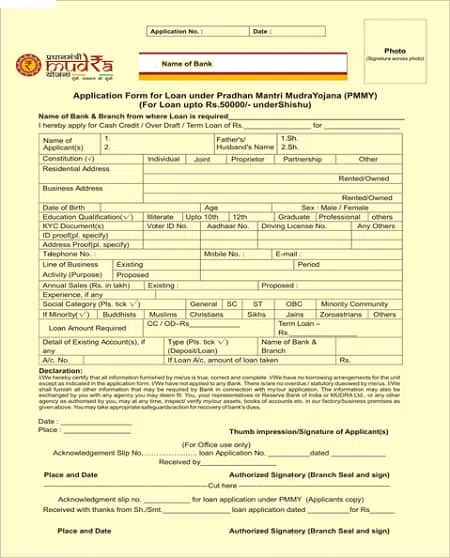

Step 1: Visit the official website of the financial institution that PMMY has authorised for you to receive the Mudra loan. Choose the appropriate form from the menu selections, which should resemble those in the screenshot below, and download it.

Step 2: Download the necessary loan application (Shishu, Tarun, or Kishore) and fill it out with your name, date of birth, residential or business address, educational background, and other pertinent personal and professional information.

Also Read: What Is Collateral and How to Get a Collateral-Free Loan?

Step 3: After that, send the application. When submitting it to the bank or lending institution, make sure you have the necessary documentation.

Step 4: The loan will be approved and deposited into your bank account after the processing and verification of the Mudra loan application form and any accompanying documents.

MUDRA Loan Eligibility

Indian residents may qualify for Mudra loans if they have unique business ideas for the service industry, commerce, or manufacturing activities and need sums up to ₹10 lakhs. Banks in the public and commercial sectors, regional rural banks, small financing banks, and microfinance organisations can provide it.

According to the requirements for MUDRA Loan eligibility, a candidate should:

|

Minimum age of eligibility |

18 years |

|

Maximum age of eligibility |

65 years |

|

Who can avail of a Mudra Loan |

Both new and existing units are eligible for loans. |

|

Security or collateral |

No security from a third party or collateral is necessary. |

|

Institutions eligible to offer Mudra Loan |

Regional Rural Banks, Public Sector Banks, Private Banks, and Micro Finance Organizations |

Interest Rate for the MUDRA Loan

The applicant’s profile determines the interest rate for the Mudra loan. The public and commercial sectors have several banks that provide MUDRA loans. Every lender must follow a set of rules; each determines the ultimate interest rate at which a borrower will get a loan. After carefully examining the applicant’s business requirements, this process is done.

MUDRA Loan Eligibility Documents:

- Identity proof includes a self-certified photocopy of a voter identification card, driver’s licence, PAN card, Aadhar card, or passport.

- Acceptable forms of proof of residencies such as Recent utility bills, property tax receipts (not older than two months), voter identification cards, Aadhar cards, and the passport of the proprietor, any partners, or any directors.

- Evidence of SC/ST/OBC/minority status

- Proof of the commercial enterprise’s identity and address like copies of pertinent licences, registration certificates, and other papers related to the business group’s ownership, identity, and location.

- Statement of accounts from the current bank, if any, during the last six months.

- Unit balance statements from the previous two years, coupled with income tax returns and sales tax returns, etc (Applicable for all cases from ₹2 Lakhs and above).

- Projected balance statements for the duration of the loan in the event of a term loan and the year in terms of the working capital limit

- Sales made up until the application deadline during the current fiscal year.

- Report on the proposed project, including technical and financial feasibility information.

- The company’s declaration, articles of association, partnership agreement, etc.

- In the lack of a third-party guarantee, the borrower’s assets and liabilities statements, including those of its directors and partners, may be requested to determine its net worth.

- Photographs of the proprietor, partners, and directors (two copies).

Also Read: Definitions and Variations of Loans and Advances

Conclusion:

On April 8, 2015, Prime Minister Narendra Modi introduced the Pradhan Mantri Mudra Yojana, which aims to give non-corporate organizations loans up to ₹10 lakhs. Under Pradhan Mantri Mudra Yojna, MUDRA Loan makes financing the credit needs of all non-farm income-generating enterprises easier. This program’s primary goal is to lend money to small and medium-sized businesses that aren’t corporations or agricultural. A mudra loan can be applied for by anybody who owns a small business.

Follow Legal Tree for the latest updates, news blogs, and articles related to micro, small and medium businesses (MSMEs), business tips, income tax, GST, salary, and accounting.