{kind=link}

A ledger is a book that contains accounts, and the classified and summarised information is posted as credits and debits. We often call it the second book of entry. It contains all the information required to prepare financial statements. It includes accounts for liabilities, assets, owners’ equity, debts, etc. The chart of accounts contains all accounts, and the ledger represents every account on the list. Now, let’s understand the general ledger meaning, examples and everything you need to know.

Did you know?

They are of two types of ledger accounts – nominal and private. A private ledger consists of confidential accounts such as drawings, capital, salaries, etc. These accounts are accessible just by selected individuals. On the other hand contains all nominal accounts, including expenses, losses, gains and incomes.

Also Read: How to Create A Ledger in Tally.ERP 9?

What is a General Ledger?

The general ledger is a master accounting document that keeps track of all of your company’s financial activities (accounts receivable and accounts payable). It allows you to see the big picture. Assets (both fixed and current), liabilities, income, expenses, gains, and losses are all accounts.

Define Ledger in Accounting

If we talk about the ledger meaning in accounting, it includes a catalogue of general accounts within an accounting system chart of accounts. Here are the main general ledger account contents:

- Asset accounts consist of the fixed asset, accounts receivable, prepaid expenditures and cash

- Liability accounts that include loans of credit and accounts payable and debt

- Equity accounts of stockholders

- Revenue accounts

- Accounts for expenses

- Loss and revenue accounts, including investment or disposal and interest.

An organisation documents the transactions throughout the year by debiting and crediting the accounts. Normal business processes trigger these transactions by charging customers or adjusting entries. The ledger account could be presented as written records when accounting is done manually and electronic accounts when accounting software applications are used.

Also Read: Journal vs Ledger: Explore the Key Differences

What is the General Ledger Accounting Balance Function?

After accepting and receiving all transactions, the ledger balance will get an update by the close of daily business. Banks determine this balance by recording every transaction, including the interest income, a deposit of funds and both-in-and-out wire transactions. It also includes the clearance check and clear debit and credit card transactions.

When you open the account on the next business day, it will reflect the balance of an account. The delays in processing deposits are due to the bank first needing to get the funds from the bank of the individual or business that issued the check, wire transfer or any other payment method. Once they transfer the funds, it becomes accessible to the account holder.

The bank statement only contains an explicit date for the balance of the ledger. Written cheques and deposits made after the date will not appear on the statement. The ledger’s balance is useful to determine whether the obligations to maintain a particular minimum balance are being fulfilled. You can also see it on bank receipts. The amount of the ledger differs from the balance of available bank accounts.

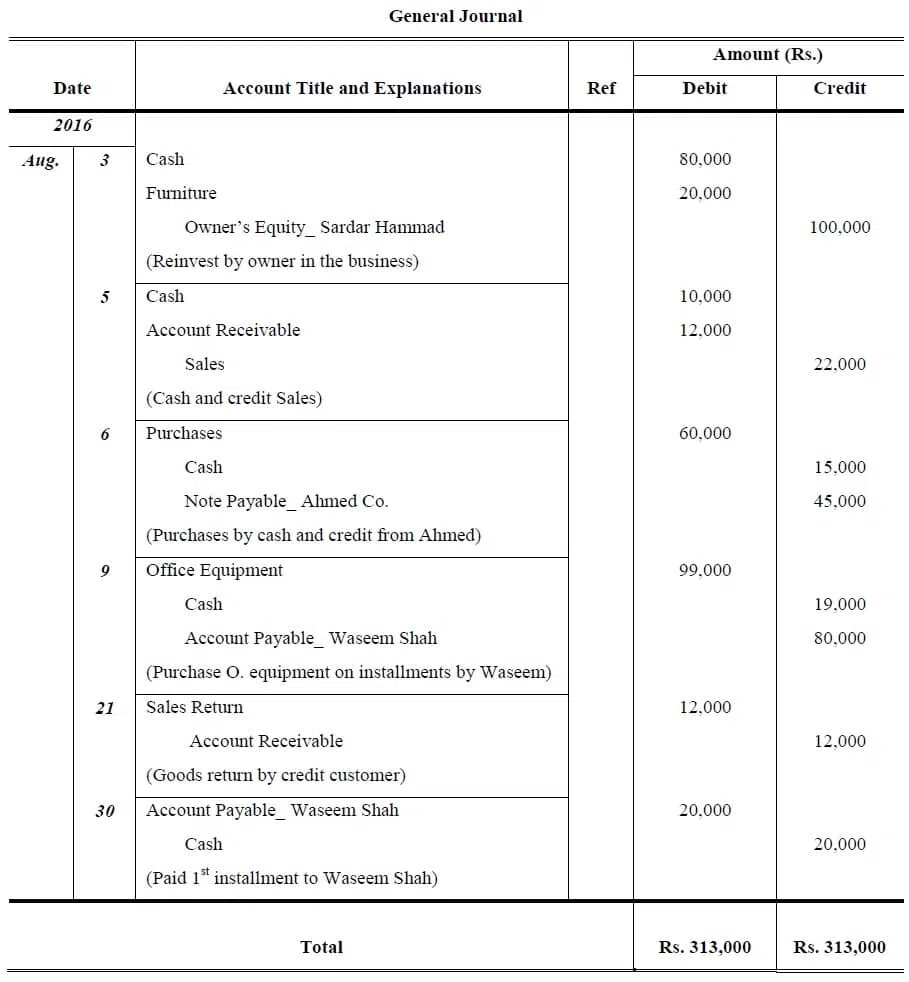

How do You Write a Ledger?

Companies that employ double-entry bookkeeping for recording transactions can create an accounting ledger. Every transaction is recorded in at least two of the accounts, including debit and credit transactions with two columns.

As a ledger account example of writing, the debit column is for credit transactions. General ledgers come in handy for businesses that employ the double-entry method, and it means every financial transaction affects at minimum two general ledger accounts.

Also, each entry includes both a credit and debit transaction. Double-entry transactions are recorded in two columns with debit postings on the left and debit entries in the middle. After that, you’ll see the sum of the credit and debit entries to see whether it’s in the balance.

Ledgers split the financial data in the journals into distinct accounts like accounts receivable, cash and sales and placed them on separate sheets. This allows you to view the specifics of your transactions.

Follow the 6 Easy Steps Below for Writing a Ledger

- Create a ledger for every account. For instance, a ledger for cash accounts will include all-cash transactions your company has. For unusual or unplanned expenses, you can create a general ledger account.

- Create columns on the left side of the page to display the journal’s number, date and description.

- Create sections on your left for credit, debit and balance. The term debt refers to the money you receive, while credit is what you owe or paid. The balance is the difference between credit and debit.

- Input the data of the journal entries into the related accounts. Put the corresponding credit and debit on top of each other. Calculate the amount you’ve got or have to pay.

- Note and alter the transactions as they happen. If you create an entry in your journal, add it immediately to the ledger.

- You can combine these accounts to create a comprehensive ledger. The front page contains an accounting chart with each account present on the list in the ledger, with the number.

The next stage of the accounting process is to establish the trial balance. You can learn the basics of accounting as well. The information in the ledger accounts is used in account-level totals in the report on the trial balance. After that, you can compare the trial balance and use them to prepare financial statements.

The Advantages of a General Ledger

- The general ledger reveals the state of the business at any point in time. For example, a cash ledger will show the amount of cash available on the date, while the bank ledger will reflect the balance in the bank.

- It helps with bank reconciliation since all the transactions for one account at a bank are present in one location.

- Additionally, as the ledgers were categorised at the time of their creation by the organisation, it is possible to look over all its debtors’ ledgers in one place.

- For auditors, the general ledger provides an overview of the transactions of an organisation. A thorough analysis of ledgers will provide auditors with a thorough understanding of the company.

Accounting’s fundamentals are journal entries, and a general ledger is the skilful arrangement and presentation of journal entries. General ledgers help organise accounting and make it easier to prepare trial balances, which help prepare financial statements.

Different Kinds of Sales Ledgers

Various ledgers are useful for a typical business. You can determine the classification by the kind of transaction you enter in the ledger.

The ledgers that are useful in the journal are as follows:

-

Sales Ledger

A sales ledger is a record of transactions that are related to sales. It provides details of the item, the amount sold, the date of transaction, whether in credit or cash and the sale value.

The data is generally maintained month-wise by most companies, and also, you can maintain the data on an annual and quarterly schedule. The volume of transactions is minimal; however, the transaction’s value is significant.

Ledgers usually store only data for one company, and the data of subsidiary companies, when they exist, are kept separate. A sub-ledger for sales made on credit is also kept to maintain an independent sales record. Inspire demand from the businesses for who the sale was can be accessible in credit.

-

Purchase Ledger

All businesses require items as raw materials to process, manufacture and distribution, in lesser amounts like selling ledgers. The ledger includes specifics about the item bought and the date, cost, quantity and other details.

Organisations keep ledgers every month, quarterly, or half-yearly based on the regularity of the purchases. Also, you must identify that a sub-ledger for all purchases is essential to maintain a separate account of transactions when you purchase with credit. This can be very helpful in identifying the due dates and amounts so that interest charges on late payments won’t take place.

-

Cash Ledger

It includes all transactions that you make in cash during a specific time. Cash transactions must need verification against bank transactions to discover how to use money properly.

The term used to match your bank’s account entries is famous as “bank reconciliation.” Typically, reconciliations are completed at the end of each month.

-

General Ledger

Transactions that don’t fit into any specified categories are included in the general ledger. It is important to ensure fewer entries, and if there are no fewer entries, it could become difficult to reconcile the entries in accounting.

Common Ledger Account Examples

A few common instances of accounts in the ledger include:

- Cash

- Inventory

- Fixed assets

- Accounts receivable

- Capital

- Debt

- Accounts payable

- Accrued expenses

- Revenue or sales

- Dividend

- Interest income

- Opex

- Administrative expenses

- Depreciation

- Taxes

Conclusion

A ledger serves as a central document for all financial transactions. You can use it to keep track of your spending and revenue by reporting expenses and income. You can also use the general ledger to compile a trial balance and spot unusual transactions, and help in creating financial statements.

Follow Legal Tree for the latest updates, news blogs, and articles related to micro, small and medium businesses (MSMEs), business tips, income tax, GST, salary, and accounting.