{kind=link}

Notices issued by GST authorities are known as GST show-cause notices. These are provided to taxpayers as a form of notification or warning about any identified defaults, particularly for the non-adherence to GST laws. Other times, notices may be issued just to receive increased information. Tax authorities will issue notices if any type of shipping or services is provided rather than being eligible for tax elimination or if taxpayers act suspiciously. They act on any information gained during the verification of the taxpayer’s GST returns and information obtained from other government departments or third parties.

Depending on the reason or degree of the default or action requested from the taxpayer, a notice may be referred to as a show-cause notice in GST, demand notice, or scrutiny notice.

Request and collection can be started for brief, non-levy, short-paid, unpaid, incorrect reimbursement, unsuitable availability, and faulty utilisation of input tax credit. All demand and recovery actions for GST begin with issuing a GST show-cause notice.

Did you know? A taxpayer must act or respond to the notices in the period provided. Not doing so can lead to putting the taxpayer in hot water. In such a case, authorities can opt to prosecute or charge a penalty for wilful default.

Show Cause Notice in GST

In the context of GST, a show-cause notice is a government document that allows an individual to explain why a specific course of operation should not be adopted against them. A person should not be declared guilty without being given the opportunity to be heard, and this is a vital part of the tax system’s procedures. It can be given for a variety of reasons, including the cancellation of registration or denial of a refund claim.

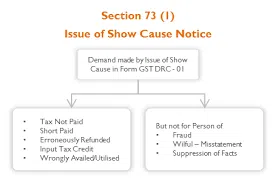

Show Cause Notice Under Section 73

For any reason other than fraud or deliberate misstatement or suppression of facts, Section 73 pertains to the identification of tax which is not paid, underpaid, or erroneously returned, or input credit claims mistakenly acquired or used.

The Proper Officer must provide an announcement for the individual mentioned above, wishing them to show cause what would lead them not to pay the sum listed in the notice, plus interest payable as per Section 50 and an imposed penalty in line with the Act’s provisions.

Show Cause Notice Under Section 74

The Proper Officer shall issue a notice on the said person needing them to show cause why they should not be questioned to pay the amount stipulated, plus interest due under Section 50, as well as 100% of the unpaid tax, short paid, erroneously refunded incorrectly acquired or employed due to some reason of fraud or any deliberate misstatement or rejection of facts solely for elimination tax.

Show Cause Notice Under Section 76

Taxes earned but not paid to the government serve as the subject of Section 76. Regardless of whether the transactions made were taxable, any amount collected “as tax” must be refunded to the government immediately under the GST Acts. If any amount due to the government is not paid, the Proper Officer may release a GST show-cause notice to the person obligated to pay the amount, mandating them to show cause why the specified amount was not paid. They should also show why a penalty equal to the amount should not be imposed on them under the provisions of this particular Section.

Also Read: Complete Guide to Job Work Under GST in India

Issuing a Show Cause Notice in GST

When an officer feels that any of the following situations involving GST income or payment for the government have occurred, this notice can be issued under GST:

- Non-levy or short levy

- Not compensated or underpaid

- Incorrect refund

- Incorrect application of the input tax credit

What is the Time Limit for Issuing Show Cause Notice?

The GST Act established a deadline for issuing show-cause notices. The time it takes to issue a show-cause notice is determined by whether the person in question is engaging in fraud or suppression.

It is evident that when a show cause notice is issued for a longer time, i.e., more than one year, owing to misrepresentation, suppression, or other reasons, the five years must be counted from the day before the notice’s issue.

What if Fraud and Suppression are Not Involved?

If the person in question is not implicated in any fraud or suppression, they can send a GST show-cause notice at least three months before the adjudication’s completion date. It must, however, decide on an issued show-cause notice within three years post the submitting date of the relevant annual return. The tax liability, interest, and penalty must all be included in the order, up to a maximum of 10% of the amount of the tax.

Cases that Involve Fraud and Suppression

If there is a possibility of fraud or suppression, a show-cause notice must be provided at least 5 months before the adjudication date. The notice must be resolved within 5 years of the exact time of filing the relevant annual return. Each order must include the tax liability, interest, and penalty for the entire amount of the tax. If the person taxable interprets their liability by themselves, they may pay it, plus interest and a 15% penalty, and notify the officer.

Recovery of Dues by the GST Department

The Government of India has several options for collecting debts from the tax evader. These include:

- Directly deducting the taxpayer’s payable amount from any refund due.

- Detention and sale of products.

- Presence of statutory provisions for the payment of debt.

- Seizing any assets owned by the tax evader.

If the GST burden remains unpaid and there is no appeal against the GST show cause notice status, the GST Department will seek to recover the tax owed.

Also Read: Late Fees and Interest on GST Return

Conclusion:

A show-cause notice in GST is a court order that asks a party to appear in court and explain why a particular course of action should not be pursued against them. This line of action is adopted if the party cannot persuade the court or fails to appear.

In several cases, the Supreme Court and high courts have condemned the practice of hearing writ petitions challenging the constitutionality of show cause notices, prolonging investigations and delaying the discovery of actual facts with the parties’ participation.

Writ petitioners will not be heard for the simple request and as a matter of routine unless the High Court is satisfied that the show cause notice was entirely honest in the eyes of the law for absolute lack of jurisdiction of the authority even to investigate the fact. These circumstances call for writ petitioners to respond to the GST show cause notice and take all of the positions stated in the writ petition before the adjudicating authority.

Do you have issues with payment management and GST? Install the Legaltree App, a friend-in-need and one-stop solution for all problems related to income-tax or GST filing, employee management and more. Try it today!