{kind=link}

Inventory means keeping a good stock of products on hand will also help you meet customer needs and prevent loss of sales. Managing inventory effectively will ensure your company can meet demand quickly. However, managing inventory can be a daunting task for many businesses.

This guide will help you understand what inventory means and how to manage it. The upcoming sections will cover the types of inventory you should consider, definitions of inventory from different perspectives, and their impact on your business.

Did You Know?

Analysts, investors and company management can all use inventory turnover to calculate how often a company sells its products in a given period. The inventory turnover can be used to determine if a company has too little or enough inventory.

Also Read: Inventory Turnover Ratio – Definition, Formula, Examples & More

What is Inventory?

Let’s start with knowing what is inventory in accounting. An inventory is anything that a business owns, whether it’s finished goods, raw materials, or priceless works of art. Inventory is also used to track the life cycle of goods, and counting items in storage is a common inventory management practice.

In addition to counting items, inventory counts also look at the condition of those goods. This information is critical in assessing stock levels and determining when to place orders. In the world of business, inventory management is essential for a successful business.

In a nutshell, inventory is a commercial document that outlines the price of goods and services and their quantity. Inventory control also play an important role in every business.

Inventory Definition: Breaking Down the Definitions

There are many definitions of inventory. Here we will look at the most common definitions in the Service and Manufacturing industries. Here are definitions of inventory from various perspectives.

-

Most Common Definition

Most people know the meaning of inventory as the value of the goods and materials owned by a business. However, there are a few different definitions of what constitutes an inventory.

In general, inventory refers to the value of work-in-process, finished goods and raw materials. It is a business’s most significant current asset, but it isn’t the only type of inventory. In some cases, it may refer to other types of assets, such as fixed assets.

-

Definition of Inventory for the Service Industry

A company’s inventory plays an important role in determining its competitiveness and ability to create value for customers in the service industry.

In the service industry, no physical stock exchange takes place. So, the inventory is generally intangible in nature. The service industry inventory generally comprises the steps before registering a sale.

Service inventories help companies increase their flexibility and productivity, allowing them to handle a broad range of customer needs without the hassle of handoffs.

-

Definition of Inventory for the Manufacturing Industry

The definition of Inventory for the manufacturing industry covers the types of items that a company needs to keep on hand to complete a particular job. Inventory for the Manufacturing industry includes all items that are either in the raw materials or finished products stage of production.

Work-In-Progress items are items that have not yet been finished but are still in the process of being manufactured. Traders may not need to classify their inventory as raw materials, work-in-progress items, or finished goods.

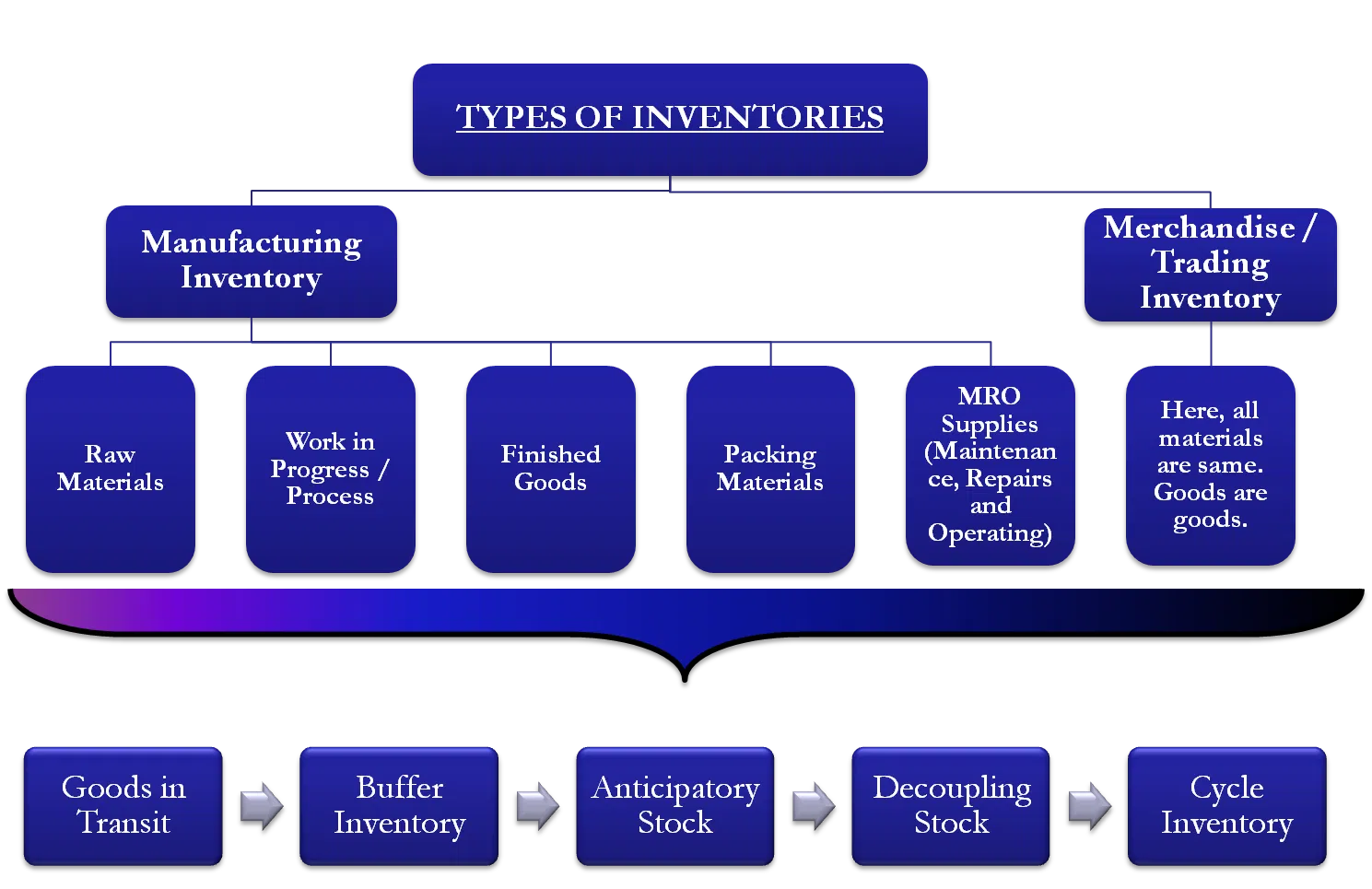

What Are the Different Types of Inventory?

After knowing the meaning of inventory, let’s know its types. In addition to raw materials and finished goods, you may also need to maintain buffer or safety stocks. These can be used for customer service purposes or to provide better customer satisfaction.

The types of inventory you maintain depend on the nature of your business, but there are several things you should keep in mind to keep your business running smoothly. This article outlines the different types of inventory and how to manage them, and it is essential to understand how these categories impact your business.

Also Read: Everything You Need to Know about Inventory Costing Methods

-

Raw Materials

In a manufacturing business, raw materials are needed to manufacture products and are recorded as a current asset on a balance sheet. This type of inventory also helps a company get bulk discounts and protects itself from market shortage situations.

It also provides a low-risk way to secure bulk discounts. Almost any manufacturing company needs to keep raw materials in inventory to manufacture products and sell them to customers. Raw materials can be classified into two types: direct raw materials and indirect raw materials.

-

Finished Goods

A finished goods inventory is an inventory that the organisation has processed, including all indirect raw materials, labour, manufacturing and administration costs.

In some cases, the organisation may incur selling and distribution costs, which are not included in the inventory valuation. In such cases, finished goods inventory is an ideal choice. However, some retailers may prefer to use a bundled inventory. The latter category can be useful for turning over deadstock but can be costly for the organisation.

-

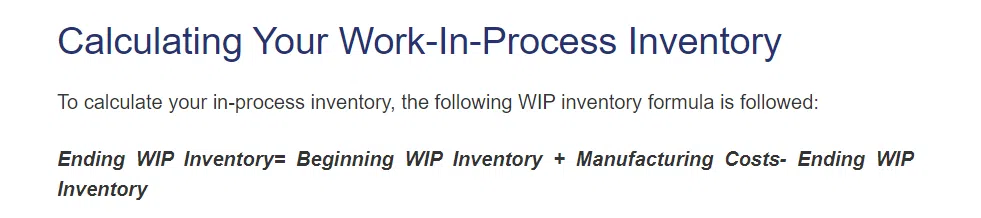

Work in Progress

If you’re looking to simplify your accounting, work-in-progress (WIP) inventory is something that you should be familiar with. If we simply explain the inventory definition in accounting, often, companies try to eliminate this inventory to simplify their books. It is often easier to quantify the value of inventory assets than work-in-progress inventories.

Work-in-progress inventory can refer to finished but unfinished products, and these items are not yet finished and take longer to complete or be transferred to finished goods. This type of inventory is commonly used in construction projects and consulting projects. A work-in-progress inventory can include any materials currently being developed or manufactured.

-

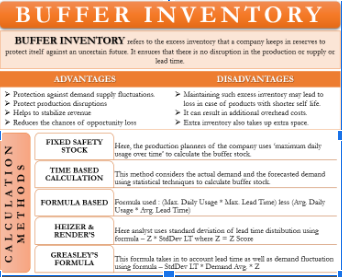

Buffer Inventory

A buffer inventory is additional inventory kept on hand when transportation delays, surges in demand, or emergencies, happen. A company can compute the level of buffer inventory by hand or use a commercial tool.

The buffer level should be a percentage of the total expected demand for a specific period of time. Ideally, a business will hold enough buffer inventory to meet the demand for half of the year.

The buffer inventory should be large enough for the company to meet the demands of its clients without causing undue inconvenience. A big buffer inventory will help the company meet client expectations and won’t tie up the company’s money.

But if the buffer inventory is too small, a company will have to invest in improved storage space. This can be costly for a corporation.

-

MRO Inventory

MRO inventory is the process of maintaining the equipment and supplies that run your production. Without MRO inventory, production stops or is delayed due to a lack of materials. In this situation, your company pays for expedited shipping and waits for a new shipment, which adds to the overall cost of repair.

Moreover, risky stopgap measures can compromise product quality or safety. By maintaining an MRO inventory, you can minimise these risks, and its main purpose is to minimise the wastage of inventory.

While MRO inventory does not generate revenue directly, it accounts for 5 to 10% of the total cost of goods sold in an organisation. Some organisations spend more than 45% of their total cost of goods. Ultimately, it represents approximately one-third of the total manufacturing budget.

-

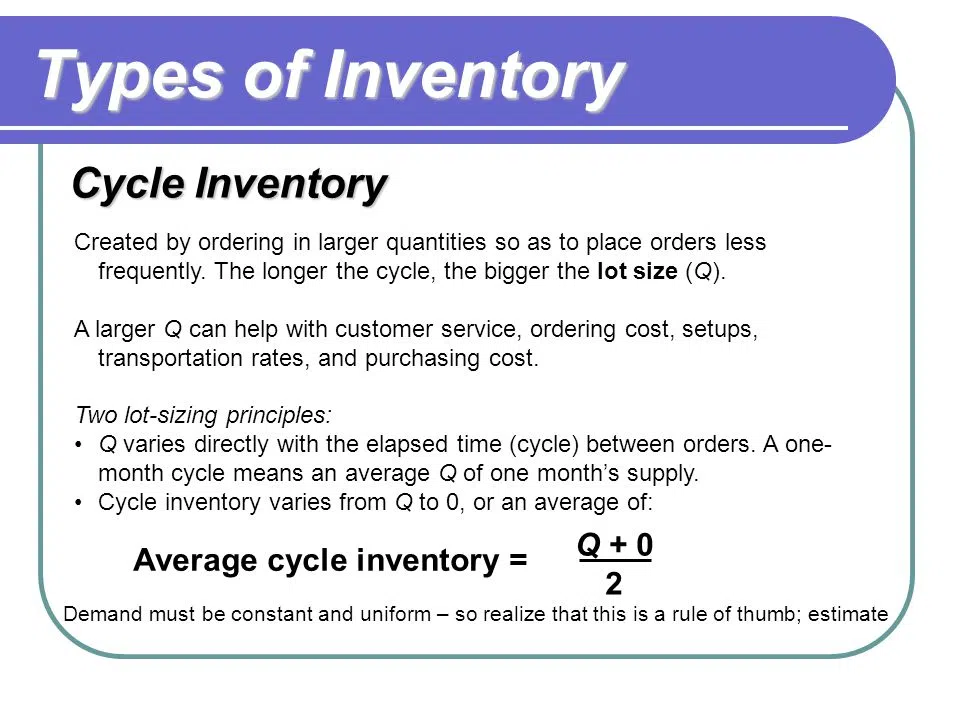

Cycle Inventory

In the case of manufacturing products, the term “cycle inventory” is used to describe the process of periodically counting all the inventory, or just a portion of it, in a specific period of time.

A cycle inventory count is usually conducted at least once during a normal sales cycle, which could be two weeks, a month, or three months. When comparing the total count of the inventory and the count from the automated system, a large discrepancy indicates a problem in inventory management. It may also be a sign of shrinkage or human error.

-

Decoupling Inventory

The concept behind decoupling inventory is simple. Decoupled inventories protect companies from unexpected circumstances that could affect their supply chain by looking at product demand and lead times. For example, it could protect them if their supplier becomes unavailable and their delivery schedule changes.

Decoupling inventory can also protect against price hikes caused by an unstable economy. By avoiding the problems caused by supply chain interruptions, decoupling inventory provides companies with a buffer against unexpected price hikes and price cuts.

What Is the Impact of Inventory on Businesses?

When inventory is not controlled correctly, a business may hurt its finances. To avoid this, businesses should periodically evaluate trends and the economy to adjust their inventory management strategies.

- Too much inventory can result in a decrease in the value of a product.

- Excess inventory has many negative effects, and it creates storage problems, takes up extra floor space and prevents the business from offering new products to its customers.

- Understocking can increase the price of a product because the business has low levels of inventory. This can be harmful to an organisation for many reasons.

- Excess inventory has an opportunity cost because it restricts the amount of money the business has available for other business opportunities.

- In addition to being a hindrance to business operations, overstocking or understocking inventory puts pressure on a business’s cash flow management.

- Excess inventory can also negatively impact a business’s profits. In addition to reducing profits, excess inventory reduces sales.

- Natural calamities and accidents can also negatively impact the business.

- Improper storage conditions can result in damaged products. Oily shelves can ruin clothing, while faulty retrieval can cause problems for an item’s fitness for production. These issues can cause major problems for a business, and staff will only be aware of the issue before production begins.

Inventory management is critical for a business. Manufacturing companies need to keep track of raw materials, safety stock, finished goods, and packing materials.

In addition to tracking these items, businesses can monitor purchasing trends and sales rates to determine the most optimal time to restock. The right inventory management practices can help improve cash flow, customer relations, and profitability while avoiding wasteful inventory and reducing unused stock.

Conclusion

So, that was all about inventory management, its various types, purposes of each type, definitions, and also its impact on your business. Now, the idea of how much and what sort of inventory to keep must be clear in your mind. You can also make use of inventory management softwares to make your work easier.

Sometimes calculations lead to a proper solution on whether your business will make a profit or not. Now keep track of your cash flow and manage your incomes and expenses with ease by using the Cashbook app by Legaltree.