{kind=link}

When you sell immovable property (besides agricultural land, building, or part of a building) to a buyer for more than Rs. 50 lakhs, the buyer has to deduct tax at source while making payment. The TDS or tax deducted at source on sale of the property is covered under section 194-IA of the IT Act, 1961.

TDS On Sale Of Property

This section contains some conditions for TDS deduction on the sale of immovable property. Here are the conditions mentioned below:

-

By Whom:

Any person can make the payment (other than the person referred to under section 194LA for compulsory acquisition).

-

To Whom:

The payment should only be made to a resident transferor, i.e. any payment to a non-resident is not covered in this section.

-

Nature Of Payment:

- The payment should be deducted from the sale amount on the transfer of any immovable property. “Immovable property” has been defined to mean any land or building or both.

- But agricultural land situated in rural areas is not considered immovable property for the purposes of section 194I. In other words, no TDS on property will be deducted in cases of transfer of agricultural land situated in rural areas even if the amount of transfer is Rs. 50 lakhs or more.

- However, “Agricultural Land”, for the purposes of this section, includes only rural agricultural land, which means that the transfer of urban agricultural land will attract the provisions under section 194-IA. In other words, TDS on immovable property is to be deducted.

Also Read: Section 194I – TDS On Rent

-

Threshold Limit:

No tax will be deducted at source if payment for the transfer of immovable property is not more than Rs. 50 lakhs (Note that this limit of Rs. 50 lakhs has to be taken individually for each immovable property. The total value of all the immovable properties transferred during the applicable financial year is required.

-

Time Of TDS Deduction:

The TDS on immovable property will be made at the time of crediting the amount to the account of the resident transferor or payment of such amount to the account of the resident transferor, whichever occurs earlier.

-

TDS Rate:

TDS is required to be deducted at 1% on the total amount of the property sale. To provide more funds to the taxpayers for dealing with the economic situation arising out of the COVID- 19 pandemic, the rate of TDS on property under Sec. 194-IA was reduced from 1 per cent to 0.75 percent for the period between 14th May 2020 – 31st March 2021.

-

Non Applicability of TDS Under Sec. 194-IA:

Since tax deduction at source for compulsory acquisition of immovable property is covered under Sec, 194-LA, Sec. 194-IA does not apply to the buyer in such cases.

-

Requirement Of TAN:

The provisions of section 203A require that every person deducting TDS shall make an application for allotment of TAN in form Number 49B. Such application needs to be made within one month from the end of the month in which tax was deducted at source for the first time. But the purchaser is not required to obtain a Tax deduction account number under Sec. 194-IA.

-

Meaning Of “Consideration For Transfer Of Immovable Property”:

Consideration for the transfer of immovable property includes the charges like club membership, car parking, electricity or water facility, maintenance, advance fees, or any other charges of similar nature related to the transfer of immovable property.

-

Requirement of PAN:

While making TDS deduction, the buyer has to obtain PAN of the seller, else TDS has to be deducted at 20 percent. The PAN of both the seller and buyer are mandatory.

-

Filing in Form 26QB:

The TDS is to be deposited using Form 26QB within thirty days from the end of a month in which TDS was deducted. After depositing TDS, the buyer has to obtain Form 16-B, which is the TDS certificate and issue the same to the seller.

Also Read: How To Make TDS Payment Online?

Example

- Mr. Amit sold his house property situated in Delhi and his rural agricultural land for a consideration of Rs. 70 lakh and Rs. 25 lakh respectively to Mr. Vasu on 02.08.2020.

- He spent Rs. 2 lakh as maintenance charges and Rs. 1 lakh as electricity charges on house property during 2018. He purchased the house property and the land in 2017 for Rs. 40 lakh and 10 lakh, respectively.

- In the given case, TDS is statutorily required to be deducted at 0.75 percent as the transaction has occurred between 14th May 2020 – 31st March 2021. Since the sale consideration of house property exceeds Rs. 50,00,000, Mr Vasu is required to deduct the TDS u/s 194-IA at Rs. 73 lakh (70 lakhs plus 2 lakhs plus 1 lakh).

- The amount of TDS would come out to be Rs. 54,750 (0.75% of 73 lakhs).

| Particulars | Amount (Rs.) |

| Agricultural land sold | 25,00,000 |

| House property in Delhi | 70,00,000 |

| Maintenance Charges | 2,00,000 |

| Electricity | 1,00,000 |

| Taxable amount | 73,00,000 |

| TDS at 1% | 54,750 |

- Nothing will be done for rural agricultural land as TDS provisions are not attracted in that case.

Also Read: TDS Challan ITNS 281- Pay TDS Online With E- Payment Tax

Steps To Pay TDS on Sale of Property Using Form 26QB

The steps for paying TDS through form 26QB are as follows:

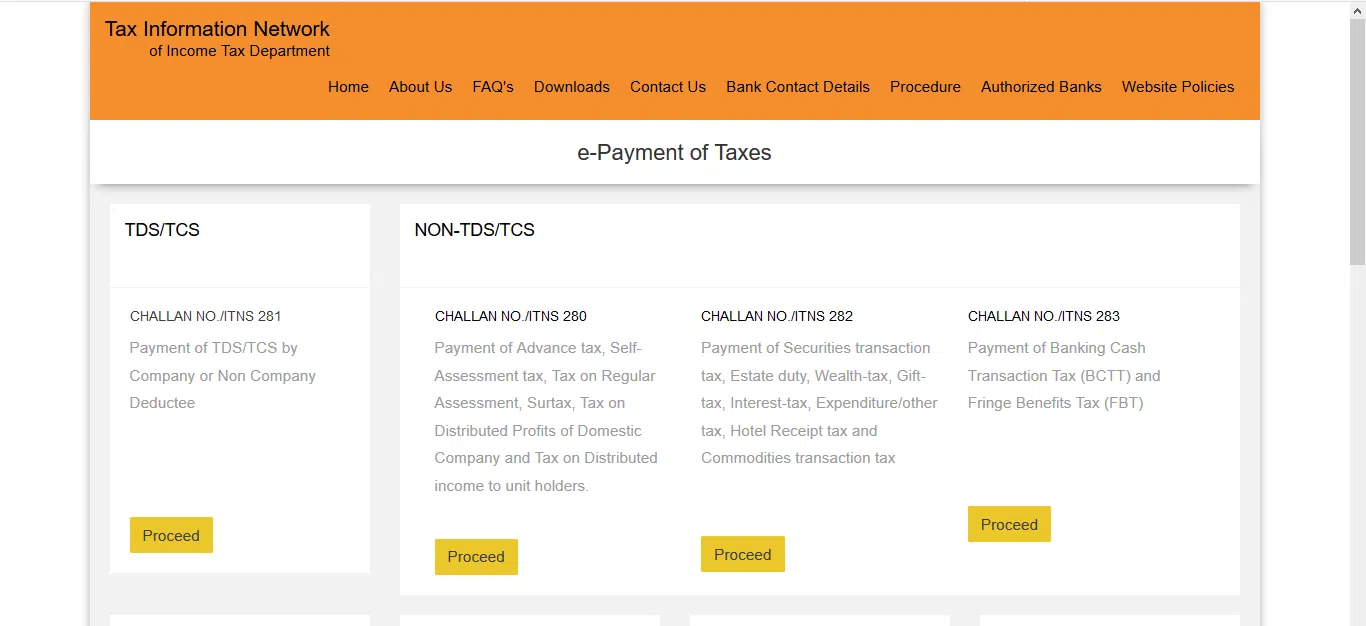

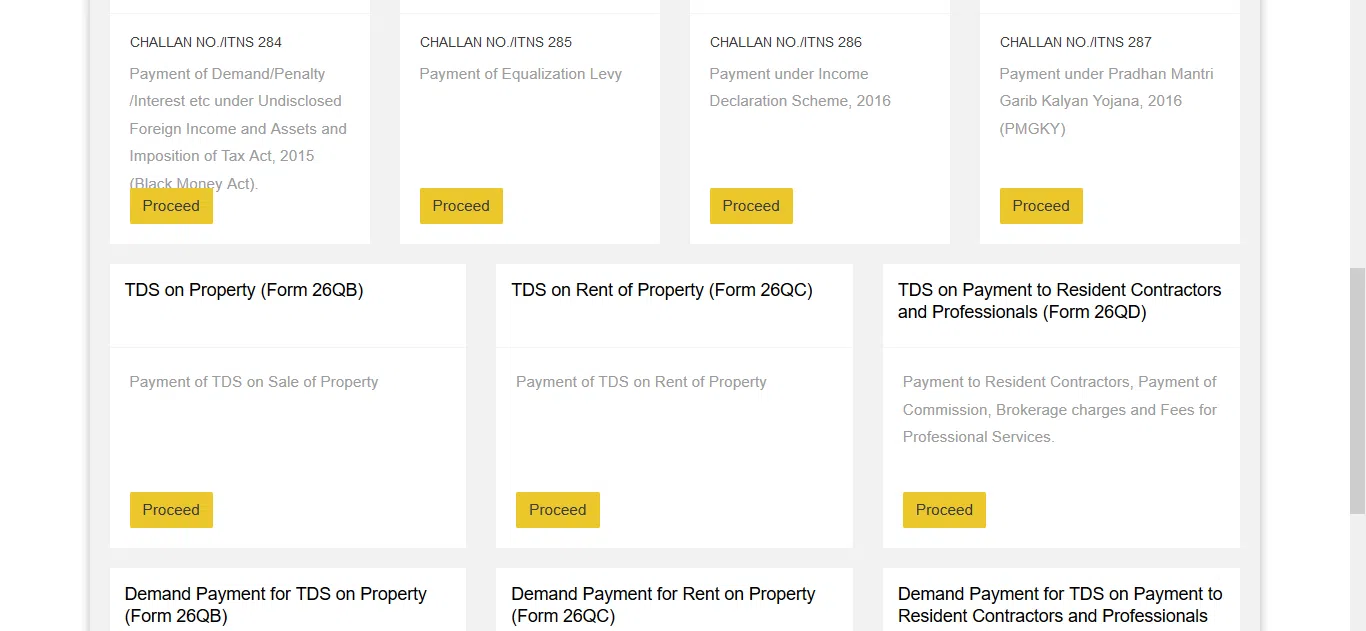

- Visit the website at https://onlineservices.tin.egov-nsdl.com/etaxnew/tdsnontds.jsp

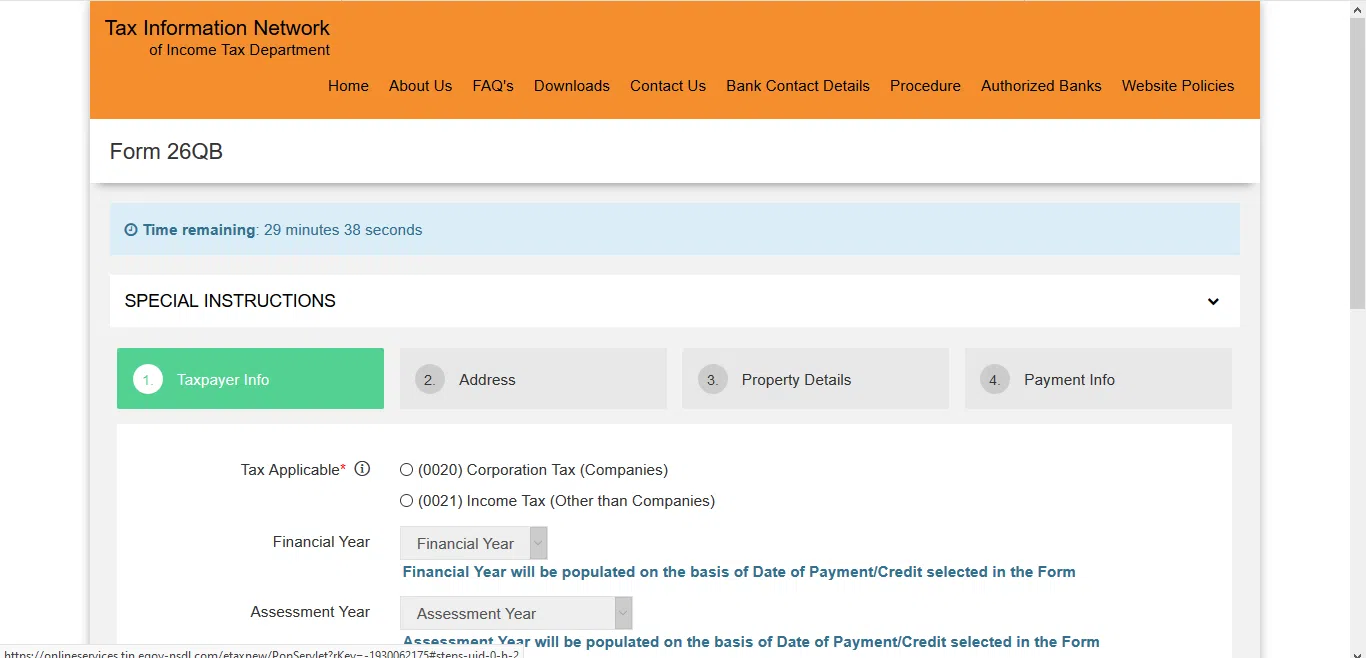

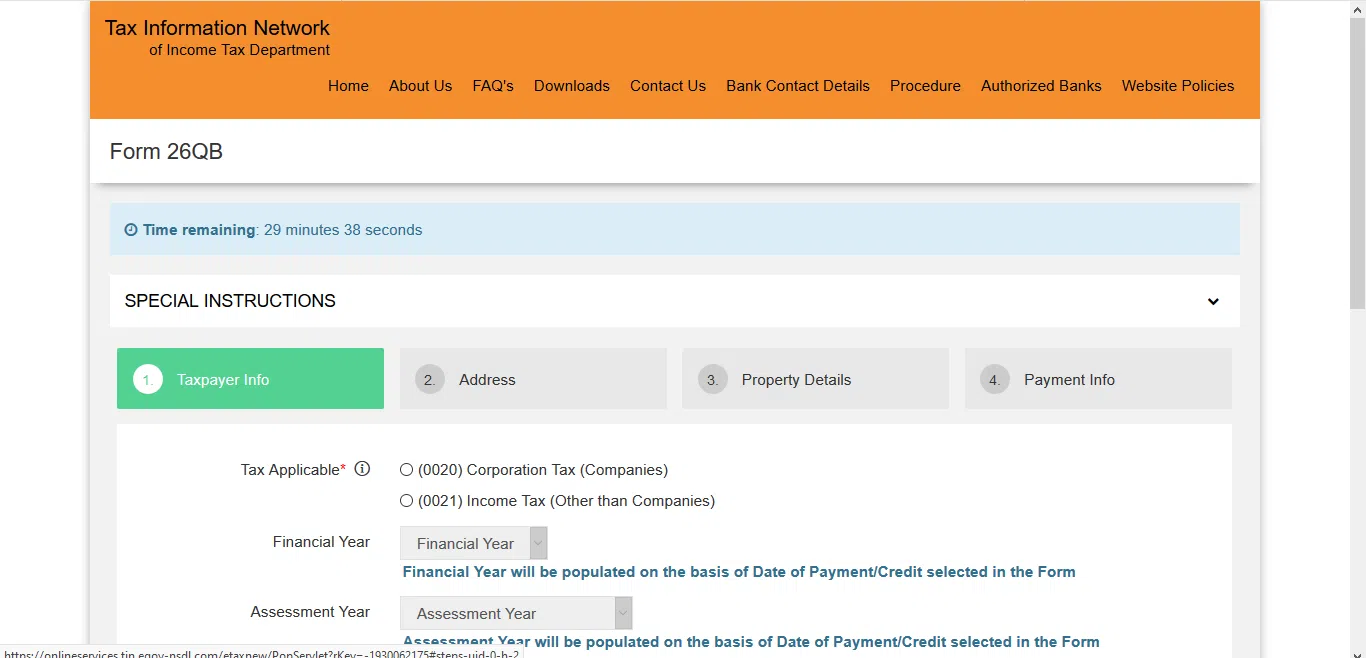

2. Click on the tab “TDS on sale of property” and proceed. A web page for form 26QB will be displayed.

3. First, you have to fill out the taxpayer information as mentioned below:

- Select the tax applicable as 0020 if you are a company and 0021 if you are not a company.

- Fill in the details of the financial year and assessment year based on the date of payment/credit selected in the form.

- Select the payment type as “TDS on Sale of Property”.

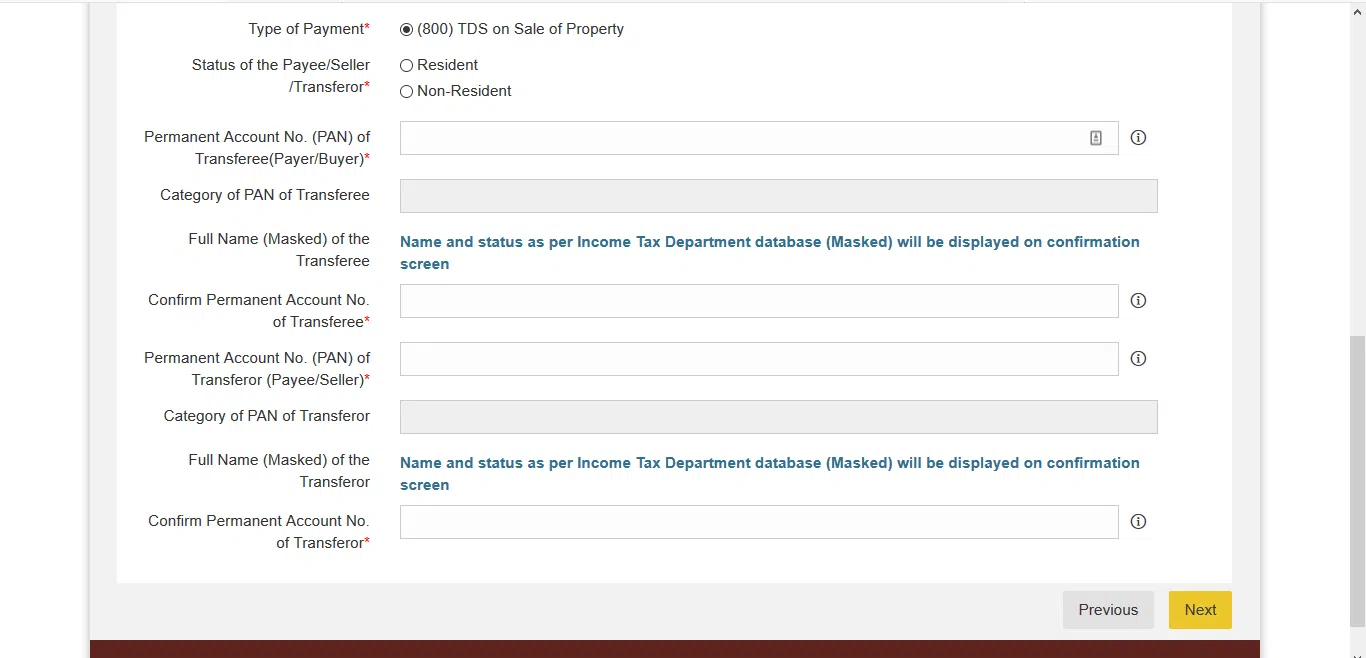

- Choose the transferor’s status, whether he is a resident or non-resident, and enter the Permanent Account Number of the transferee and the transferor.

- Proceed to the next section and enter the details of the complete address of the buyer and the seller- the name of the building, flat/block no., road, city/district, state, pin code, e-mail id, mobile number and select whether there are more than one buyers/sellers.

- Proceed to next, and the property details will appear on the screen.

- Fill out the complete property address to be transferred – the name of premises/building, flat/block number, road/street, city /district, state, pin code, date of agreement/booking, the total value of consideration and the type of payment.

- Select the amount paid/credited from the list of crores/lakhs/thousands/hundreds.

- Fill out the details of the tax deposit – TDS amount, interest, fee and the total payment to be made.

- Proceed to next, and the tab “payment information” will be displayed as mentioned below:

- Select the mode of payment as e-tax payment immediately or on a subsequent date.

- Fill in the date of payment/credit and the date of tax deduction and submit the filled form to proceed further.

- The site will display a confirmation screen. After the confirmation, a screen will appear showing two options as “Print Form 26QB” and “Submit to the bank”. It will also show a unique acknowledgement number on the screen. It is preferable to retain this acknowledgement number for future purposes.

- Click on “Print Form 26QB” if you want to print the form. Then press “Submit to the bank” to make the payment online through internet banking. Then proceed to the payment page via the internet banking facility provided by various banks.

- When the payment is successful, a challan appears on the screen containing details regarding Challan Identification Number, payment amount and bank name. This challan is proof that payment has been made.

Also Read: Challan 280 : How To Pay Your Income Tax Online With Challan 280

Registration In TRACES for Filing Correction Statement

The registration on TRACES is compulsory to file a “Correction Statement”. It helps in filing the corrections. Once you are officially registered, you can utilise various facilities provided by TRACES. You may also view TDS /TCS credits, verify form 16, look into the refund status, etc. There are some simple steps to get registered in TRACES as mentioned below:

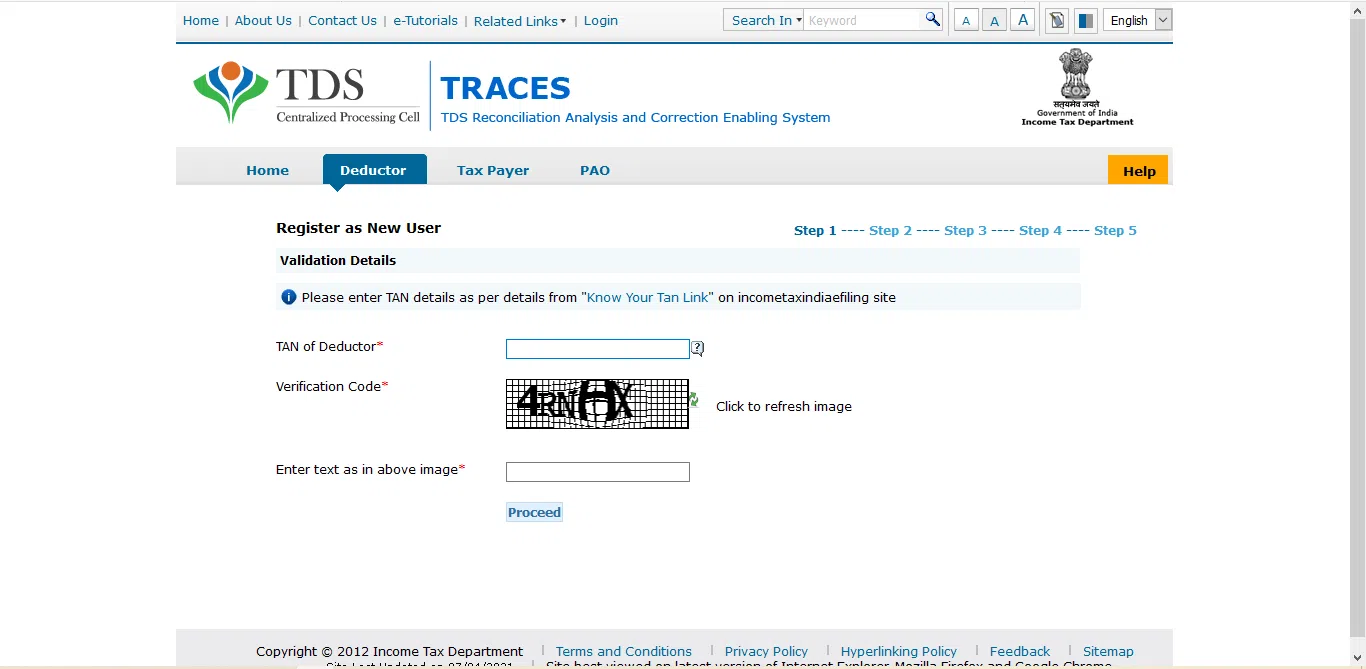

- Step 1: Go to https://contents.tdscpc.gov.in/. Select the tab “Register as a New User”, and choose the type of user as Deductor, and click Proceed.

- Step 2: Enter the Temporary Account Number of the deductor registering on TRACES, fill the text as displayed in code and proceed further. If you require any details, click on the help icon.

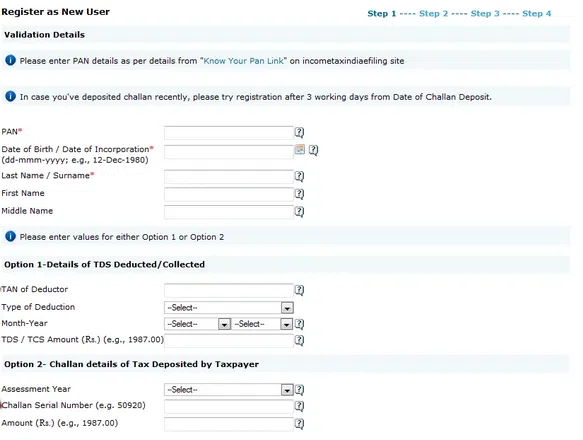

- Step 3: Enter the Token number of the Regular Statement filed for the financial year, quarter and form type, along with CIN/BIN and PAN details.

- In PART 1, enter the Challan Identification Number (CIN) details: BSR code /Receipt number, the date you deposited tax, Challan serial number, Challan amount/transfer voucher and CD record number (not mandatory).

- In PART 2, enter the unique PAN – amount combination for the challan/transfer voucher. Try entering three distinct PAN – amount combinations and fill the TDS deposited for respective PAN’s and click on proceed.

- Step 4: The authentication code is generated after validation of KYC, which will remain valid for the calendar day for the same form type, financial year and quarter. You can now proceed with the code, TAN, and the name of the already filled deductor. You need to update your PAN and other details.

- Step 5: The Deductor must create a User ID and the Password and click the ‘Create an Account button.

- Step 6: A confirmation page will appear on the screen. Check all the details regarding your communication address as well as phone number and e-mail id. Click on “Edit” if you want to modify the details, and then click Confirm to continue further.

- Step 7: Finally, you will receive the message that your Registration request is successfully submitted. You will receive the activation link and codes to the email address and mobile number provided during registration. After activating your account, registration will be completed successfully, and you can log in to TRACES.

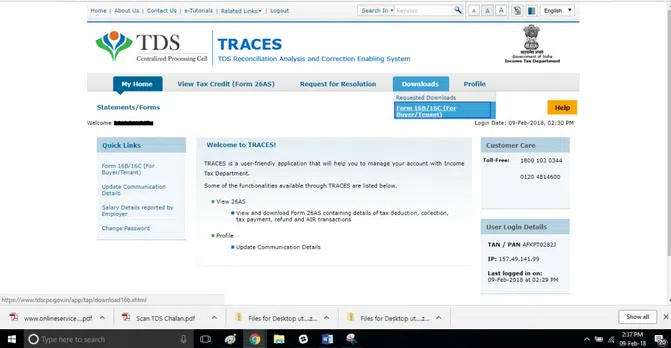

Downloading Form 16B:

- Login to the TRACES portal at www.tdscpc.gov.in as a taxpayer.

- Select “Form 16B (For Buyer)” under the Downloads tab.

- Fill in all the details regarding the property transaction for which Form- 16B is initiated. Enter the applicable Assessment Year, an Acknowledgment Number, Permanent Account Number of transferor and press “Proceed”.

- TRACES will display a screen seeking confirmation. Press “Submit Request” to proceed further.

- A message on the submission of the download request as successful will be displayed on the screen. Note the request number to search for the download request.

- Press “Requested Downloads” to download the files which you requested.

- Search for the request with the generated requested number. Select the row to be requested and proceed by clicking on the “HTTP download” button.

Notice For Non- Filing OF FORM – 26QB

Where the person responsible for deducting and paying TDS to the government fails to do so, such person shall be deemed to be an “assessee in default”. When a buyer fails to deduct TDS using Form- 26QB or pay the applicable tax to the government for a transaction worth more than 50 lakhs, the Income Tax(IT) Department sends a notice regarding the same to the buyer. The immediate step is to deposit the tax with a late fee and interest to avoid the penalty.

Penalty

Suppose the buyer has failed to deduct the tax or deducted the tax but failed in depositing the same to the government after receiving the notice from the income tax department too. In that case, he will be liable to the penalties given below:

-

Penalty u/s 201

Section 201 of the IT act, 1961, imposes a penalty on the person who has failed to deduct TDS or to deposit the tax to the government. The penalty regarding the same will be charged as under:

- At a simple interest of one per cent for every succeeding month or part of each succeeding month will be charged on the total amount of default for the delay starting from the due date on which such TDS should have been deducted till the date on which such TDS was deducted, and

- At a simple interest of one and half per cent for every succeeding month or part of each succeeding month on the total amount of default on account of late payment of TDS deducted to Govt. starting from the due date at which such tax was deductible till the actual date of payment of such deducted tax.

* The fraction or part of the month will be considered as a full month.

-

Penalty u/s 234E

Section 234E states that where a person fails to file a TDS return on or before the due date, he must pay the late fee penalty of Rs. 200 for every day during such default lasts. The actual amount of late fee penalty will be lower of the following:

- TDS Amount or

- Delay in number of days* 200

For example, if the aggregate amount of TDS is Rs. 20,000 and there’s a delay of 129 days, the late fee will be 129 * 200 = Rs. 25,800. Lower of Rs. 20,000 and Rs. 25,800 is Rs. 20,000, and hence the maximum late fee penalty payable will be Rs. 20,000

Also Read: Income tax Calculator – Calculate Your Taxes For FY 2021-22 Use Tax Calculator Online