{kind=link}

Goods and Services tax is the indirect tax that is levied on goods and services in India. Although it is paid to the government by the seller, it is finally borne by the consumer using such goods and services. Every business needs to get itself registered under GST law if its aggregate turnover exceeds the GST registration limit.

What is Aggregate Turnover Under GST?

As per section 2(6) of the CGST Act, Aggregate turnover is the total value of all taxable supplies which is used to calculate the threshold limits for GST registration. It is also the key to determine whether a taxpayer is eligible for the composition scheme.

It includes all exempt supplies, exports of goods or services, and inter-state supplies of persons having the same Permanent Account Number, calculated on an all-India basis.

However, It excludes the inward supplies on which RCM (reverse charge mechanism) is paid.

Also Read: A Brief Guide To Reverse Charge Under GST

Importance of Aggregate Turnover Under GST

Before explaining how to calculate the same, let’s first understand the relevance of the aggregate turnover in GST law.

- The concept of aggregate turnover for calculating the GST registration limit has improved the tax collection.

- Using the aggregate turnover system, the previously exempted companies have also now come under GST.

- Also, the government can inspect businesses and make them register under the GST law. This has expanded the taxpayer base too.

How to Calculate the Aggregate Turnover for Calculating GST Limit?

Aggregate Turnover is required to calculate the GST registration limit and check whether the supplier must register for GST registration. We always take into account the previous financial year figures while calculating the aggregate turnover of the entity.

It can be calculated as below :

For an individual with the same Permanent Account number across all his business organizations across India, aggregate turnover is :

Value of all taxable supplies, exports, exempt supplies, Inter-State supplies

MINUS

Taxable Value of supplies under reverse charge mechanism, inward supplies, non-taxable supplies of goods or services like alcohol, petrol, etc.

Let’s take an example.

Maya owns an agricultural estate in West Bengal which has an annual turnover of Rs. 2 crores. This business is exempt from tax. But she also charges for the bags for the supplies of such produce. The turnover from the sale of such bags is Rs. 4 lakhs which is liable to GST. Should Maya register under the GST law?

The answer is YES. When you consider whether a person needs to register under GST law, we consider the aggregate turnover and not the taxable turnover. Also, the agriculture estate is in West Bengal which is a normal category state. Hence, the total aggregate turnover of Maya, including the exempted turnover, is greater than the threshold limit for GST registration of Rs. 40 lakhs.

In short, a taxpayer even if exempted from paying tax has to comply with GST registration rules provided his aggregate turnover exceeds the required limit.

Also Read: GST Calculator Online Goods and Services Tax Calculator

Job work and Aggregate turnover

One point to be noted is that the supplies of goods that take place after the completion of the job work will not form part of the aggregate turnover for a job worker. The examples of such supplies are :

- Return of goods to the Principal

- Goods are sent to another job worker on the instruction of the Principal.

- Goods which are supplied directly by the principal from the premises of the job worker.

Aggregate Turnover vs Turnover in a state

Many people confuse the aggregate turnover under GST with the turnover in a state. Both are distinct from each other. Now that we have defined aggregate turnover above, let’s understand what we mean by turnover in a state.

- Turnover in a state means the total volume of business done by the entity in a year. It will include the following:

- All supplies between different states and entities.

- All taxable supplies excluding the ones on which reverse charge is applicable.

- Export supplies

- All exempt supplies under GST.

- All taxes excluding GST taxes.

- Any goods received from the job worker as a principal.

- Any goods supplied to job worker as a principal.

- Any supplies of job worker on behalf of the principal.

- Aggregate turnover is calculated to calculate the threshold limit for GST purposes and the eligibility of the taxpayer for the composition scheme.

- On the other hand, turnover in a state is needed to calculate the Composition levy under the composition scheme that is to be paid to the government. In other words, turnover in a state is taken into account and not aggregate turnover to calculate the composition levy charge to be paid.

- The composition levy is a reduced tax alternative designed for small taxpayers. Under this scheme, the small taxpayers, if eligible, need to pay GST only at a fixed specified rate of turnover. Also, taxpayers get the option of filing quarterly returns instead of monthly.

Which Are the Normal Category States For Calculating Aggregate Turnover?

GST is a destination-based tax, and it is received by the state in which such goods and services are used and not where they are manufactured. Some states opted for the new threshold limit for GST registration and while others opted for the existing limits of GST registration. The states include the union territories as well. These are listed below :

Normal category states

New registration limit

Following are the states and the union territories that opted for the new GST registration limits, i.e., the new limit of Rs 40 lakh :

- Delhi

- Bihar

- Kerala

- Gujarat,

- Haryana,

- Punjab,

- Chattisgarh,

- Goa,

- Uttar Pradesh,

- Andhra Pradesh,

- Himachal Pradesh,

- Jharkhand,

- Odisha,

- Tamil Nadu,

- Rajasthan,

- West Bengal,

- Lakshadweep,

- Dadra and Nagar Haveli,

- Chandigarh

- Andaman and Nicobar Islands

Existing registration limit

Normal category states that remain with the existing GST registration limit, i.e., of Rs 20 lakhs

- Telangana

Also Read: GST State Code List and Jurisdiction

Which are Special Category States while Calculating Aggregate Turnover?

Aside from the normal category states, there are certain special category states in GST. A special category state is the one that enjoys a special status given by the Centre to help such state in its growth and development. These states face certain limitations like hilly terrains, infrastructure backwardness and international borders.

So they are not able to grow at the same rate as other states. Hence Centre gives them special assistance in such regard. That’s why the threshold limit for GST is low in these states as compared to normal category states. Like the normal category, these states also can change to a new threshold limit for GST registration. Again these are also divided into two parts :

|

GST REGISTRATION LIMIT |

SPECIAL CATEGORY STATES |

|

New registration limit of Rs 20 Lakhs |

Jammu and Kashmir Ladakh Assam |

|

Existing registration limit of Rs 10 Lakhs |

Puducherry Meghalaya Mizoram Tripura Manipur Sikkim Nagaland Arunachal Pradesh Uttarakhand |

What is the GST Registration Limit?

- Recently there have been certain demands from MSME (Micro, Small and Medium Enterprises) to increase the threshold limit for GST registration. Under this, the states can either go with the existing GST registration limits or the newly introduced GST limits.

- Under both cases, limits are separate for normal category states and special category states. A point to be noted is that these new GST registration limits introduced are only for providers of goods and services and not service providers. In other words, the GST limit for services remains the same.

Limits for GST Registration

Existing Limits Of GST Registration Up to March 31, 2019

- If the aggregate turnover under GST exceeds Rs 20 lakhs for the supplier in normal category states, then registration is compulsory.

- If the aggregate turnover under GST exceeds Rs 10 lakhs for the supplier in special category states, then registration is mandatory.

New Threshold Limit For GST Registration From April 1, 2019 (Optional For States )

(Only For Sale Of Goods )

- If the aggregate turnover exceeds Rs 40 lakhs for the supplier in normal category states, GST registration is mandatory for such a supplier.

- If the aggregate turnover exceeds Rs 20 lakhs for the supplier in special category states, GST registration is compulsory for such a supplier.

Also Read: Latest GST News, Information, Notifications & Announcements

Non- Applicability Of New GST Registration Limits

According to the Centre, certain suppliers even if their aggregate turnover exceeds Rs 20 lakhs they have to compulsorily get themselves registered under GST law. Such suppliers are not applicable for the new registration limit of Rs 40 lakhs:

- Those who are involved in manufacturing and supply of tobacco or tobacco manufacturing substitutes.

- Those who supply or manufacture ice creams or other edible ice without considering whether it contains cocoa or not

- Those involved in the manufacturing and supply of Pan Masala.

GST Registration Limit Under Composition Scheme

Under the Composition Scheme, the limit varies depending on the taxpayer category. The annual turnover is checked for the preceding financial year while checking their eligibility for registration. Following are the different GST rates applicable to different taxpayers:

|

TAXPAYER |

Traders and Manufacturers |

Restaurant Service Providers |

Other Service Providers |

|

Old Annual Turnover |

Rs 1 crore |

Rs 1 crore |

– |

|

New Annual Turnover |

Rs 1.5 crore |

Rs 1.5 crore |

Rs 50 lakhs |

|

GST rate |

1% |

5% |

6% |

How GST Registration Benefits Different Groups

- For the Government, GST registration allows them to identify taxpayers and ensure tax compliance efficiently.

- To suppliers of goods and services, for availing input tax credit on tax paid on the sold goods and services and using it to set off output tax on goods and services.

- Recognition of the supplier of goods and services as the legally authorized seller of such goods and services for customers

- There is a transparent, seamless flow of goods and services and input tax credit for the market.

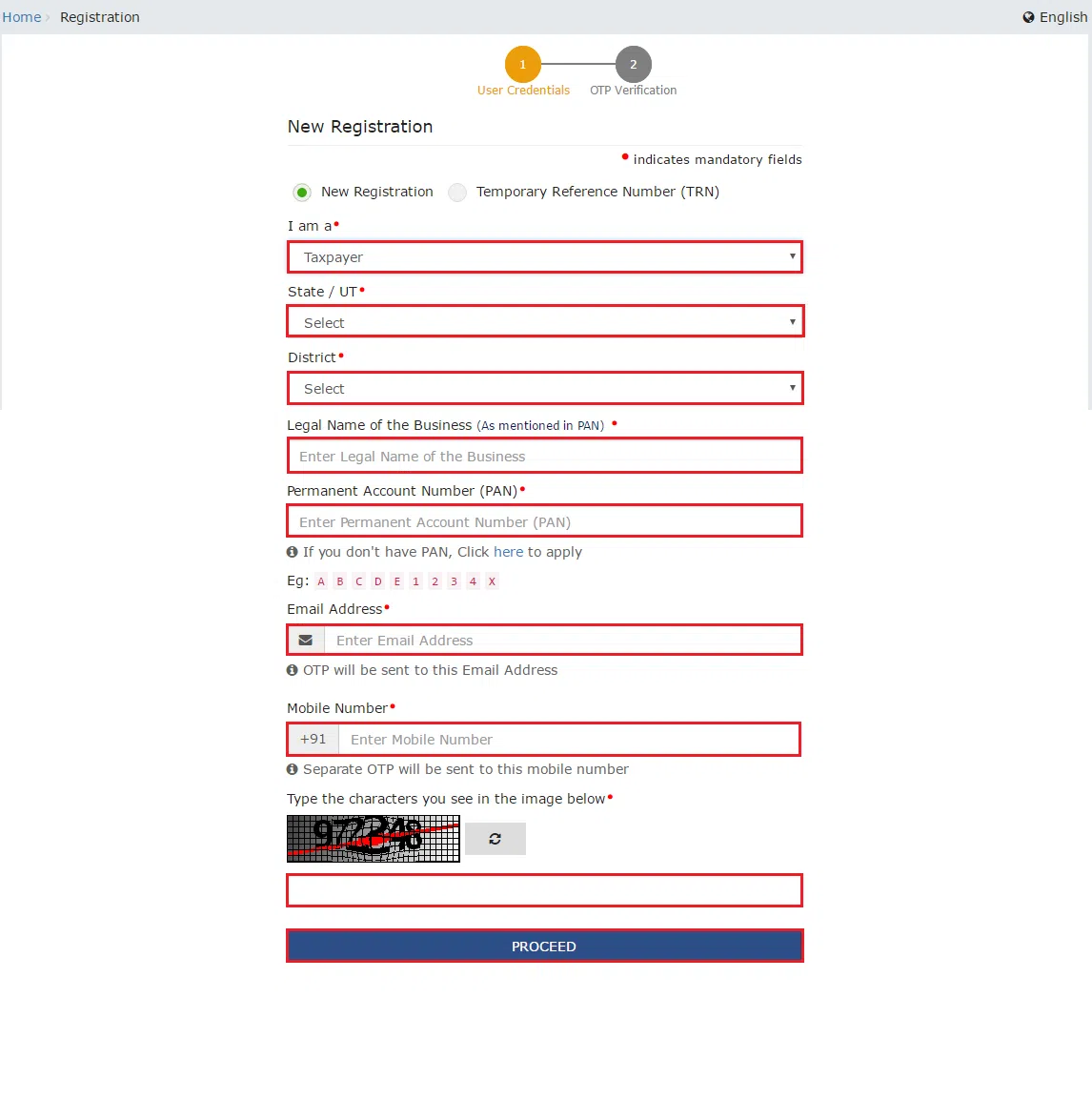

How To Register For GST

It is very easy to register yourself for GST.

- Go to the official GST portal of the government of India www.gst.gov.in

- Next, click on the services and go to the Registration.

- Click on the new registration under the Registration tab. Enter your PAN, other details and click on submit. On the next page verify the OTP and register.

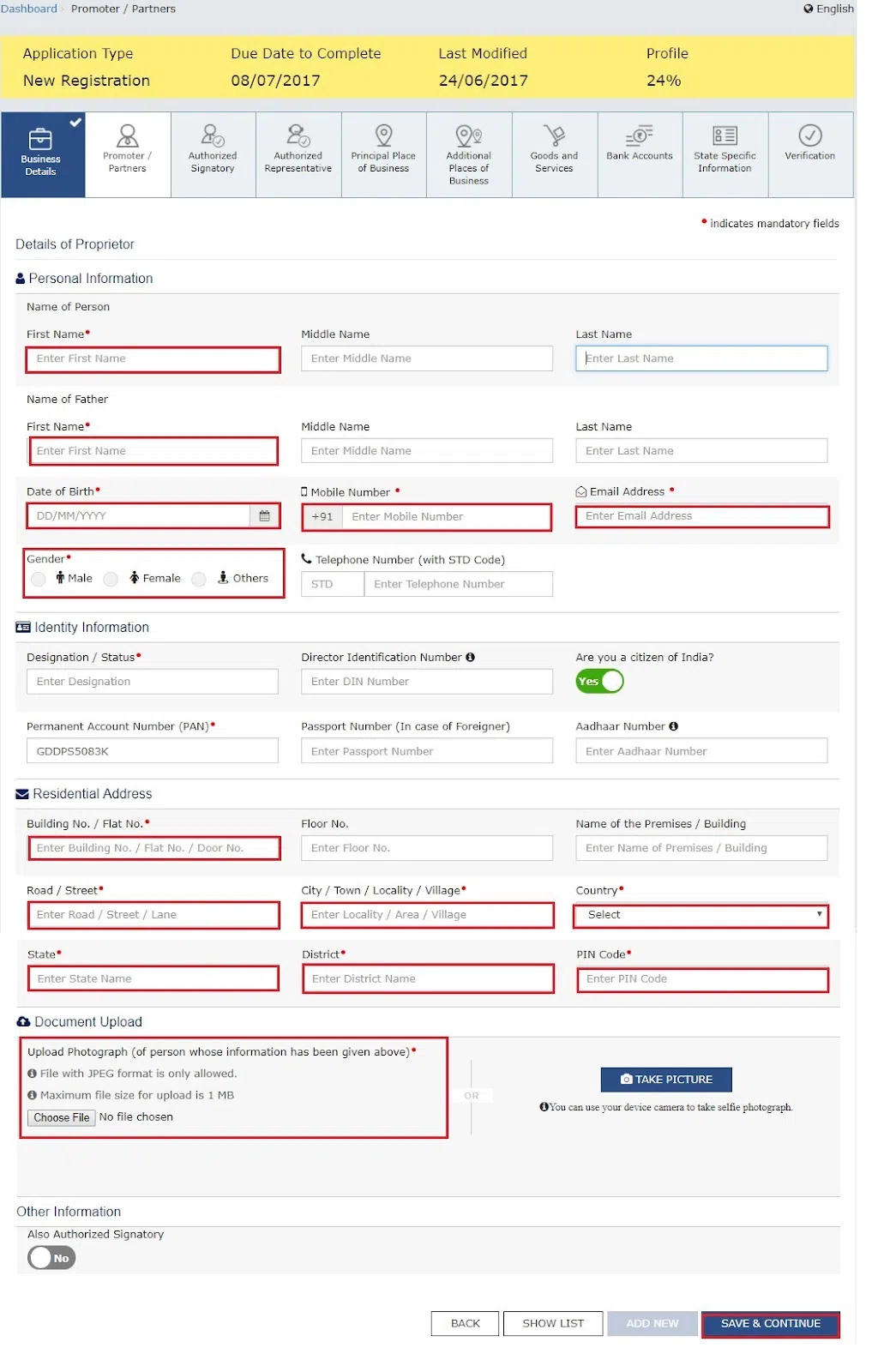

- Once you verify the OTP, a TRN or temporary reference number is generated. Log in to the portal again with that TRN, go to your dashboard, click on saved applications and complete your application.

- To complete the application, you will be required to attach the proof of business incorporation, bank account statement, Photo and address proof of the taxpayer, and a digital signature.

Once the government verifies the application, the Central Government issues a unique 15 digit registration number known as GSTIN. You can download your GST Certificate by logging into the GST portal.

Remember that each state needs a separate registration number. If you operate from more than one state, you need to obtain the registration number from these states.

Also Read: GSTIN Importance, Format & How to Apply for GST Number

Mandatory GST Registration

The Centre has listed down certain persons who must register under GST law as per Section 24 of the CGST Act, 2017, irrespective of whether the taxpayer is eligible as per the threshold limit for GST registration or not. Following is the list of such persons :

- Casual Taxable persons mean those who have no place of business but act in the capacity of principal or agent when occasionally involved in the supply of goods and services.

- All those required to pay tax under reverse charge mechanism, i.e. unlike normal GST, the tax is paid by the person supplying the goods and services.

- All individuals who are liable to pay tax u/s 9(5).

- Non-resident taxable persons. In other words, a person who is not a resident of India or has a place of business in India. If they want to start any business in India, they need to apply for a minimum of 5 days before starting such a business in India.

- All such individuals, who are involved in transactions related to an inter-state taxable supply.

- Input Service Distributors

- Any business that supplies online information or retrieves information services from outside India to a non-registered person in India.

- All such supplies operated through an e-commerce operator, i.e ., all such supplies other than mentioned under section 9 sub-section 5, to a person other than the registered person in India.

- Persons recommended by the GST council and notified by the government to get themselves registered under GST law.

Exemption From GST Registration Under Section 24 Of CGST Act

All such individuals who are involved in supplies of handicraft goods with an aggregated turnover of Rs. 40 lakhs are exempted from registration under this Act. Such a limit of Rs. 40 lakhs will be revised to Rs. 20 lakhs for special category states like Manipur, Nagaland, Tripura, and Mizoram.

Penalty for Non-registration

If you are liable to be registered under GST Law and fail to do so, you will be penalised under the GST law by the relevant authorities. Such taxpayers will be liable to a penalty of Rs 10,000 or the amount of tax evaded, whichever is higher.

Conclusion

After reading the above article we hope you have a fair understanding of what is aggregate turnover and how to calculate the same to know whether you need to get yourself registered under GST law or not. If you have any further doubts and queries about the GST limit or GST turnover limit, you should connect with GST experts or chartered accountants and take their professional advice.